24 Jul 2023

24 Jul 2023

Transparency in Crypto Exchange Fill Volumes (Updated July 21, 2023)

Introduction

Analyzing the health of various crypto markets and exchanges from an external perspective can be quite a daunting task. A cursory glance at token and exchange metrics on platforms like CoinMarketCap or CoinGecko may give the impression that the trading volume has only slightly declined since the peak of the last bull run in 2021. However, it is essential to recognize that this apparent stability in volume figures is a result of significantly overstated volume data that exchanges provide to market aggregators.

This inflation of volume data is influenced by several factors, including exchanges artificially boosting volume through internal trading desks to improve their rankings on aggregator websites and attract more users to their platform. Additionally, exchanges impose minimum trade volume requirements, unsustainable trading competitions, and other pressures on token issuers to inflate volume or face delisting. Unethical service providers also contribute to the issue by offering wash trading services under the guise of legitimate market-making, leaving issuers unaware that these practices do not contribute to genuine volume. As a result, there has been a notable reduction in price speculation and retail participation within the crypto industry, leading to a substantial decline in trading volumes during the ongoing bear market.

In this blog post, we aim to shed light on Acheron's relative fill volume from the beginning of 2022 to the end of May 2023. This data will provide an estimate of the overall relative change in volume within the long-tail digital asset industry. Notably, as Acheron served as a counterparty in all of the fill volume transactions, we can confidently assert the data's integrity, safeguarded against the overstatements frequently observed on popular market aggregators and exchanges directly. By presenting accurate and reliable insights, we aim to improve professionalism and provide valuable information to the crypto community amidst the challenges of assessing market health.

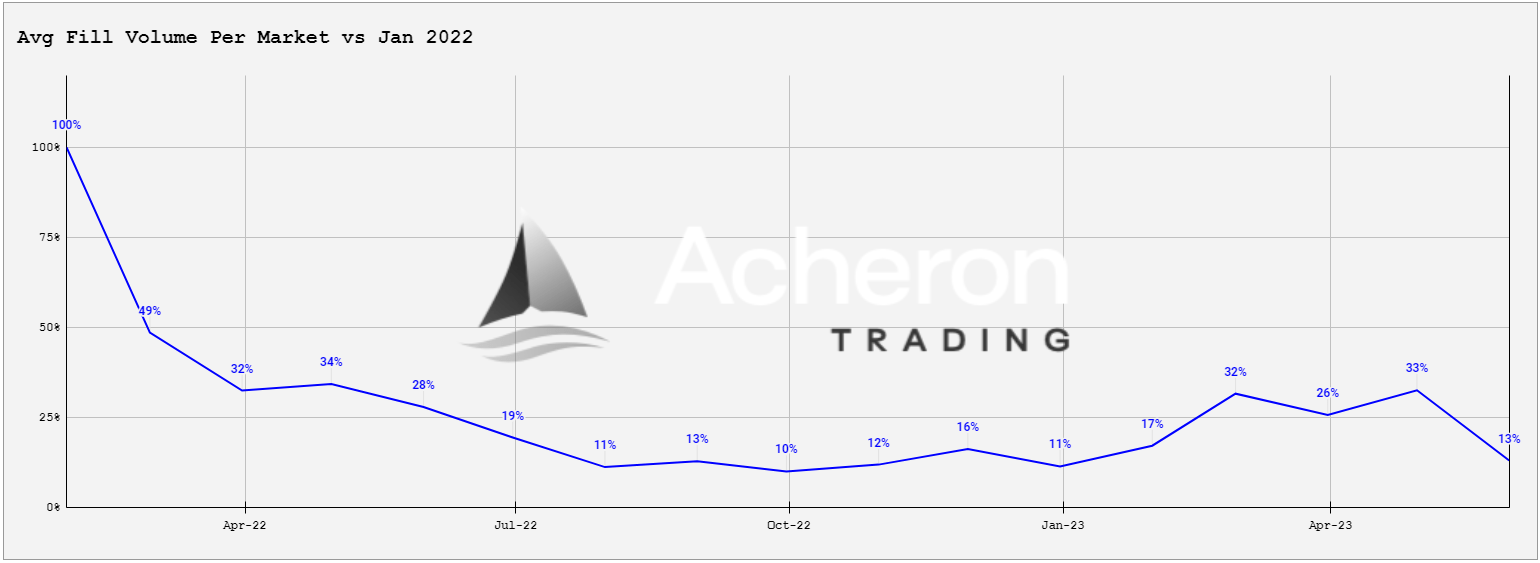

The chart above provides a comprehensive view of the changes in average fill volume per month since January 2022. To gain valuable insights, it is crucial to analyze the data on a per-market basis, allowing us to account for any variations in the quantity of market Acheron traded in. Several key takeaways emerge from this analysis:

January 2022 marked the highest average volume of any month throughout the observed period, indicating strong market activity at the beginning of the year.

In contrast, September 2022 recorded the lowest average market volume of any month, with a meager 10% of the average market volume witnessed in January 2022. This significant decline indicates a considerable drop in trading activity during that specific month.

Subsequently, there was a notable increase in average market volume at the start of 2023. However, this surge was short-lived, as the average market volume plummeted to just 13% in May, falling back to levels comparable to those seen from July to December 2022.

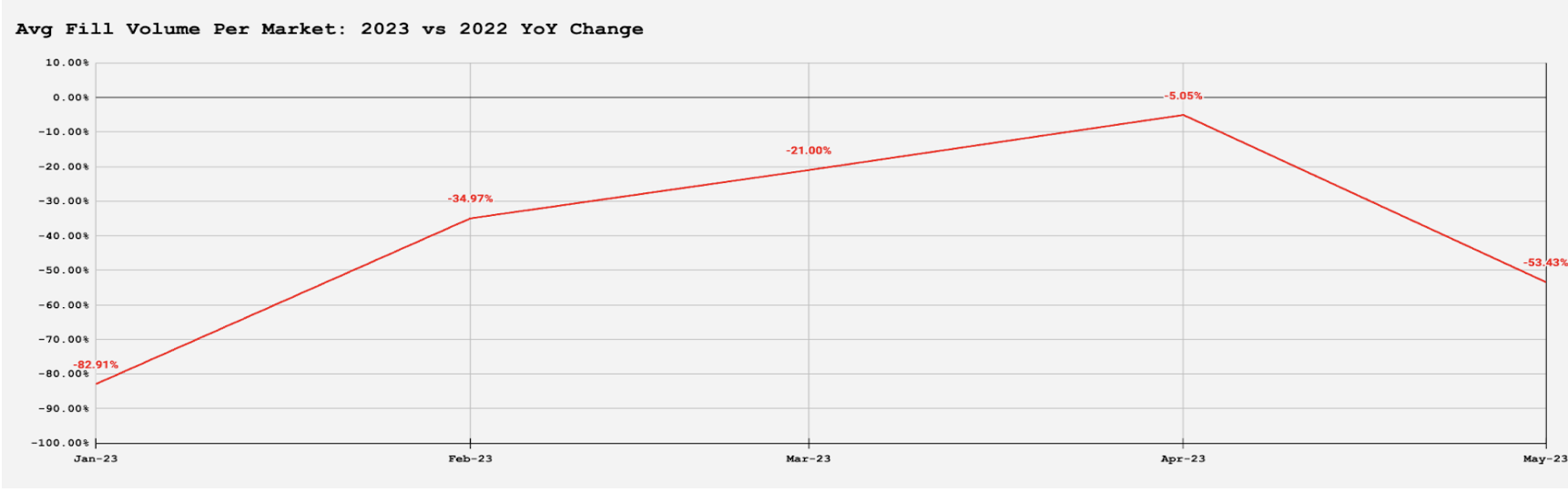

Examining the year-over-year changes, it becomes evident that the precipitous drop in volume has persisted, even after considering seasonal factors. Specifically, the average market volume in January 2023 was substantially lower, experiencing an 83% decrease compared to the same month a year earlier. Additionally, the last recorded month, May, saw a significant 53% decrease compared to its counterpart in the previous year. These stark declines in volume can be primarily attributed to fundamental factors, such as decreasing outside liquidity and deteriorating macroeconomic conditions, rather than mere seasonal flows.

By focusing on these detailed analyses of average fill volume per month, we gain a deeper understanding of the trends and challenges that have impacted market conditions.

Relative Volume Data by Exchange

Understanding relative volume data by exchange is crucial in assessing their performance compared to their peers. The table provides insight into the last three months' average fill volume per market per exchange relative to the leading exchange in each specific month:

Exchanges | May | Apr | March |

Binance | 100% | 100% | 100% |

Kraken | 41% | 6% | 9% |

OKX | 21% | 62% | 19% |

Kucoin | 21% | 15% | 32% |

Bybit | 10% | 8% | 23% |

Coinbase | 9% | 16% | 7% |

Ascendex | 9% | 3% | 9% |

Gate.io | 7% | 4% | 11% |

Bittrex | 2% | 2% | 3% |

Huobi | 2% | 0% | 2% |

Bitmart | 1% | 1% | 4% |

As expected, Binance stands out as the clear volume leader in all three months, maintaining a significant margin over other exchanges. Despite facing regulatory challenges in the US and Europe, Binance remains the preferred platform for altcoin trading and retains its position as the only true tier 1 exchange.

An essential point to consider concerning Coinbase is that its volumes often overlap with Binance, meaning that markets available on Coinbase are likely to be present on Binance as well. Our strategies are designed to maximize flow, making Coinbase's volume relatively lower, although the month-to-month differences are still relevant.

Tier 2 exchanges include OKX, Kucoin, Bybit, and Coinbase, executing between 6% to 62% of Binance's volume in any given month. This wide range is influenced by one market on OKX experiencing unusually high volume, well beyond its normal range. Excluding this outlier, the range changes to 6% to 32%, with an average expected volume of 17% relative to Binance.

The remaining exchanges can be classified as tier 3, with Gate.io and Ascendex occasionally performing at a level comparable to a tier 2 exchange. Understanding these tiers based on relative volume data allows us to gain valuable insights into exchange performance.

What to Look for in a Market?

When evaluating a market, several essential factors should be considered to ensure its viability and potential for trading:

1. Liquidity Management: One of the primary indicators of a healthy market is deep liquidity. It's crucial to assess the depth within 2% of the order book and observe spreads lower than 1%. While volumes are important, liquidity metrics such as order book depth and uptime should be given higher priority, especially during bearish conditions.

2. CoinPaprika's Combined Orders/Volume Statistic: CoinPaprika's CO/VOL % can serve as a valuable rule of thumb to identify artificial trading interactions within a market. A generally high CO/VOL % indicates a liquid market, with figures over 100% suggesting highly favorable liquidity. On the other hand, low CO/VOL % values raise concerns about lower liquidity, and figures below 5% are particularly concerning.

By focusing on these aspects when evaluating a market, traders can make informed decisions and identify potential opportunities for trading. Deep liquidity and efficient market conditions are essential factors to consider, especially during bearish market conditions. For example, a high volume asset with a depressed valuation might look attractive for an opportunistic trader, however if there is no liquidity, the opportunity is a mirage. In contrast, a low volume asset with a depressed valuation might look uninteresting, however if there is robust liquidity in the asset, low volume may just be a genuine reflection of the current market conditions and not the underlying fundamentals which could present a seizable opportunity. Think about exchange reported volume as the cover of a book, but liquidity as the real story.

Key Takeaways

In light of a significant 87% decline in volume since January 2022, with the majority of remaining volume often concentrated on one exchange, asset issuers must strategically position themselves for success. To navigate this challenging landscape, it is crucial for issuers to exercise a high level of selectivity when choosing their listing partners, whether for primary or secondary exchanges.

While Binance rarely engages in primary listings and follow-on listings are limited to high-performing projects, issuers should consider alternative options such as OKX, Coinbase, Bybit, Kucoin, and to a lesser extent, Gate.io and Ascendex, considering their volumes. However, they must carefully weigh the listing costs and requirements of each exchange. Simply focusing on the exchange with the highest volume may not be the most sensible approach, as volume is not always correlated with market quality.

For issuers seeking a follow-on listing, it is vital to ensure that the new venue represents a clear upgrade over any existing exchanges. Adding a new venue comes with increased working capital commitments for the project, and given the current environment of low exchange volumes and challenging fundraising conditions, issuers must be cautious not to burden themselves with exchanges that offer little value-add. It may be more prudent to maintain the status quo than to opt for a lateral listing if a higher-tiered exchange is not a feasible option.

In these market conditions, issuers can also leverage good negotiation tactics, armed with the true volume conditions on centralized exchanges. Exchanges should demonstrate a willingness to work with issuers during a downturn and foster long-term win-win relationships. Unlike the take-it-or-leave-it offers of the previous bull cycle, the current climate offers an opportunity to use market cycles to one's advantage.

Lastly, it is important for issuers to remember that periods of low volume are a normal part of the crypto macro cycle. As highlighted in Acheron's December 2021 blog post titled "Flood Warning," the last stage in a recessionary cycle, following a prolonged period of exuberance, is characterized by "a period of low volatility and stagnation...followed by smart money accumulation" before a new cycle begins. Given the strength demonstrated by BTC and ETH after their 2022 lows, it appears that the alt coin market is currently in the midst of this phase.

By implementing a strategic and selective approach to listing partners, carefully evaluating the benefits of follow-on listings, employing effective negotiation tactics, and acknowledging the cyclical nature of the crypto market, asset issuers can position themselves for success in low-volume environments.

An AI-Generated Summary

Analyzing crypto markets and exchanges requires caution due to overstated volume data provided to market aggregators.

Acheron's analysis shows a significant decline in true market volume compared to reported figures, impacting price speculation and retail participation.

Key takeaways from the analysis:

January 2022 had the highest average volume, while September 2022 had the lowest.

Average market volume surged at the start of 2023 but dropped back to 13% in May, similar to levels seen in July-December 2022.

Year-over-year changes show substantial volume declines in January 2023 (83%) and May (53%).

Exchange data shows Binance as the leading exchange with high volumes, followed by tier 2 exchanges like OKX, Kucoin, Bybit, and Coinbase.

Essential factors to consider when evaluating a market include deep liquidity, CoinPaprika's CO/VOL %, and liquidity and market efficiency.

Key takeaways for asset issuers in low-volume crypto markets include exercising selectivity in listing partners, considering alternative exchanges, ensuring new venues offer clear upgrades, using negotiation tactics, and understanding the cyclical nature of the crypto market.

Contact

If you are interested in this information and would like to discuss more, please feel free to reach out through our contact form.

THE CONTENT ON THIS WEBSITE IS NOT FINANCIAL ADVICE

The information provided on this website is for information purposes only and does not constitute investment advice with respect to any assets, including but not being limited to, commodities and digital assets. This website and its contents are not directed to, or intended, in any way, for distribution to or use by, any person or entity resident in any country or jurisdiction where such distribution, publication, availability or use would be contrary to local laws or regulations. Certain legal restrictions or considerations may apply to you, and you are advised to consult with your legal, tax and other professional advisors prior to contracting with us.