02 Dec 2021

02 Dec 2021

Flood Warning

I'm accelerating this period's update as November has brought a massive surge in primary listing performance and catalyzed a flood of new tokens entering the market.

To recap our conclusion as we closed October, I mentioned:

"As we look at the current conditions for primary listings as an indicator of overall market health, we are trending back towards exuberance territory marked by both a surge in first-day pop's as well as significant quote deltas. However, we see more outlier performance, meaning traders are still allocating selectively among projects they perceive as the highest quality. Selectivity is an important attribute. If the market reaches total exuberance where everything is "up only," many low-quality participants will flood the market with supply. Such events exhaust retail demand and could lead to another recessionary cycle that we saw play out earlier in the year."

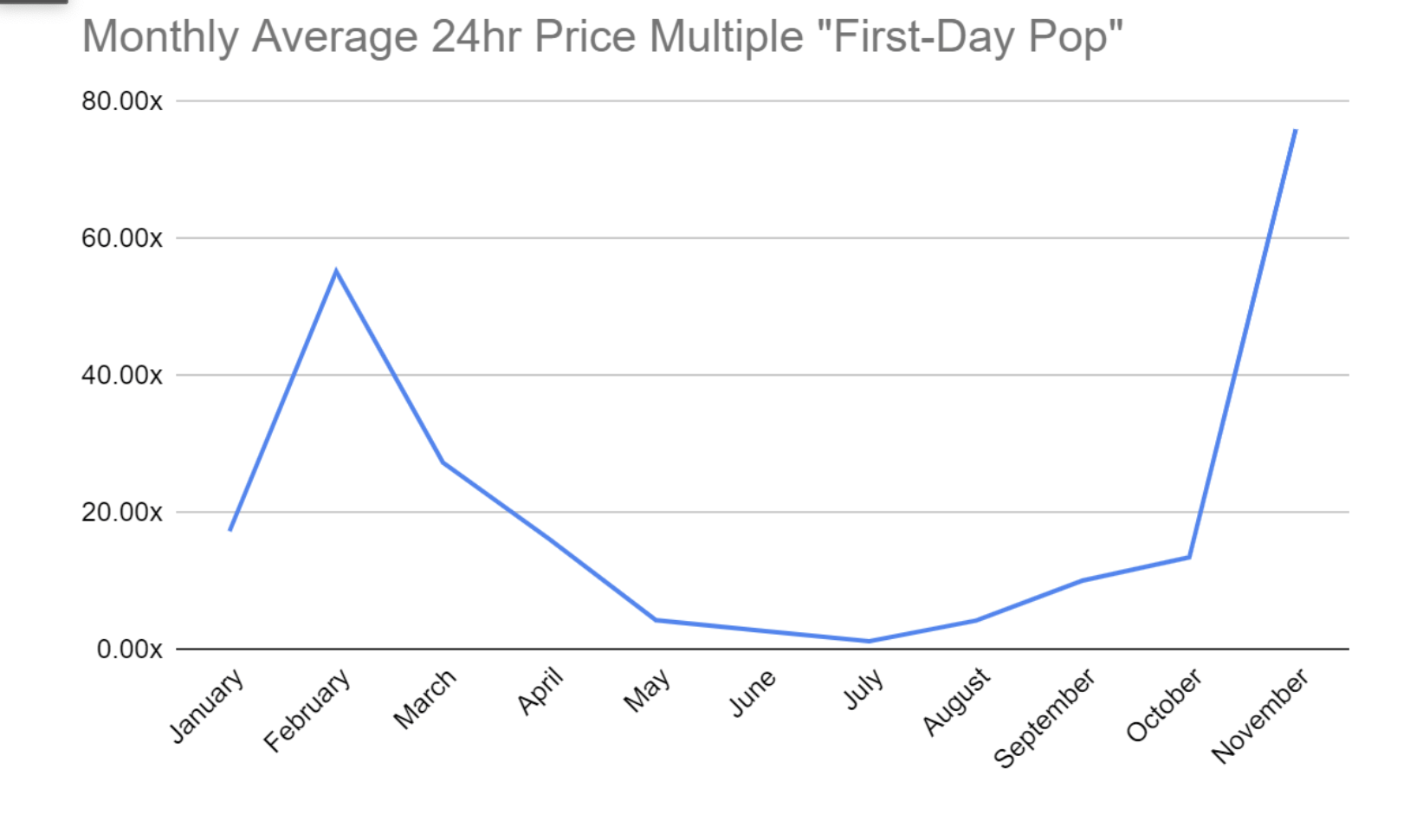

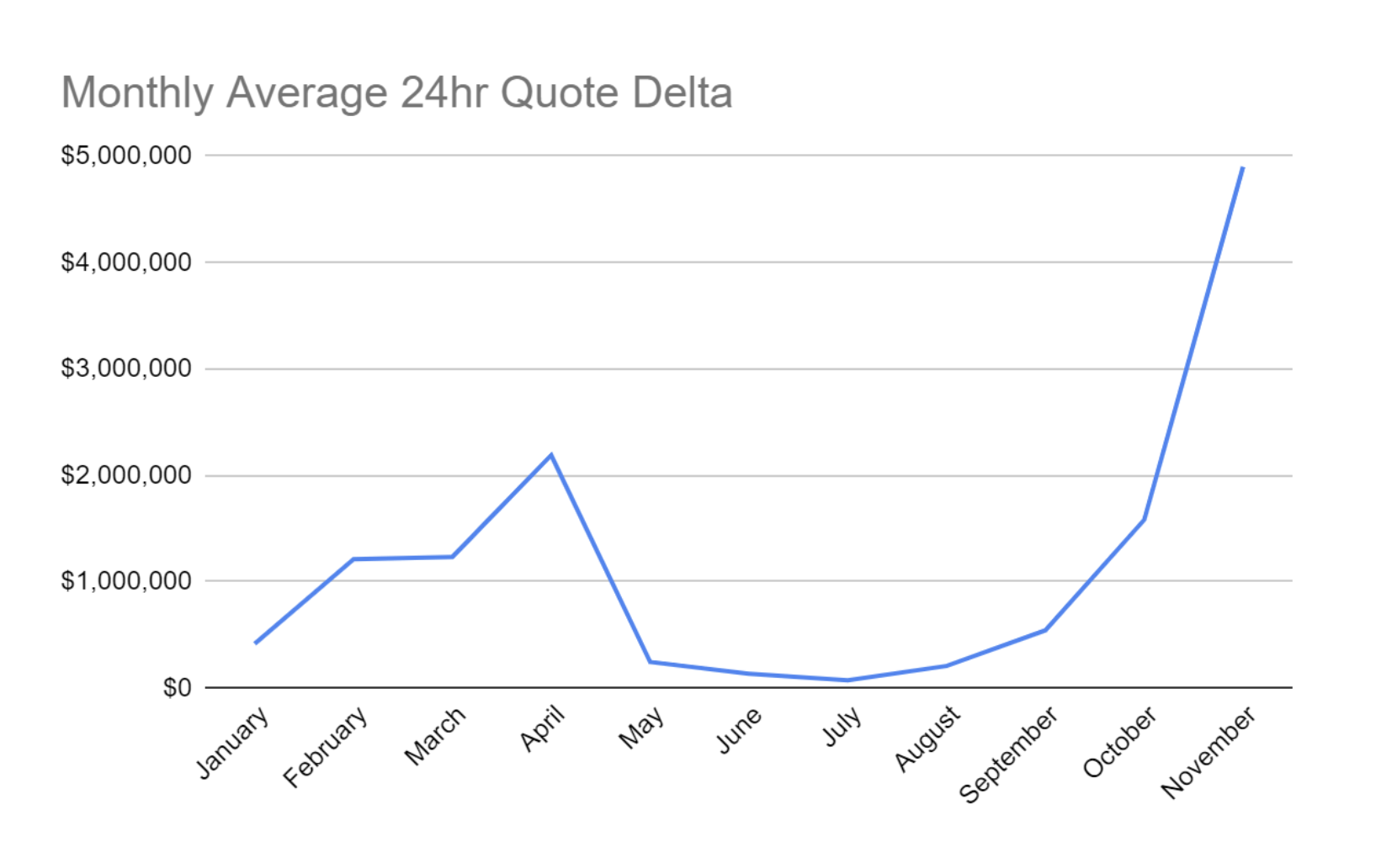

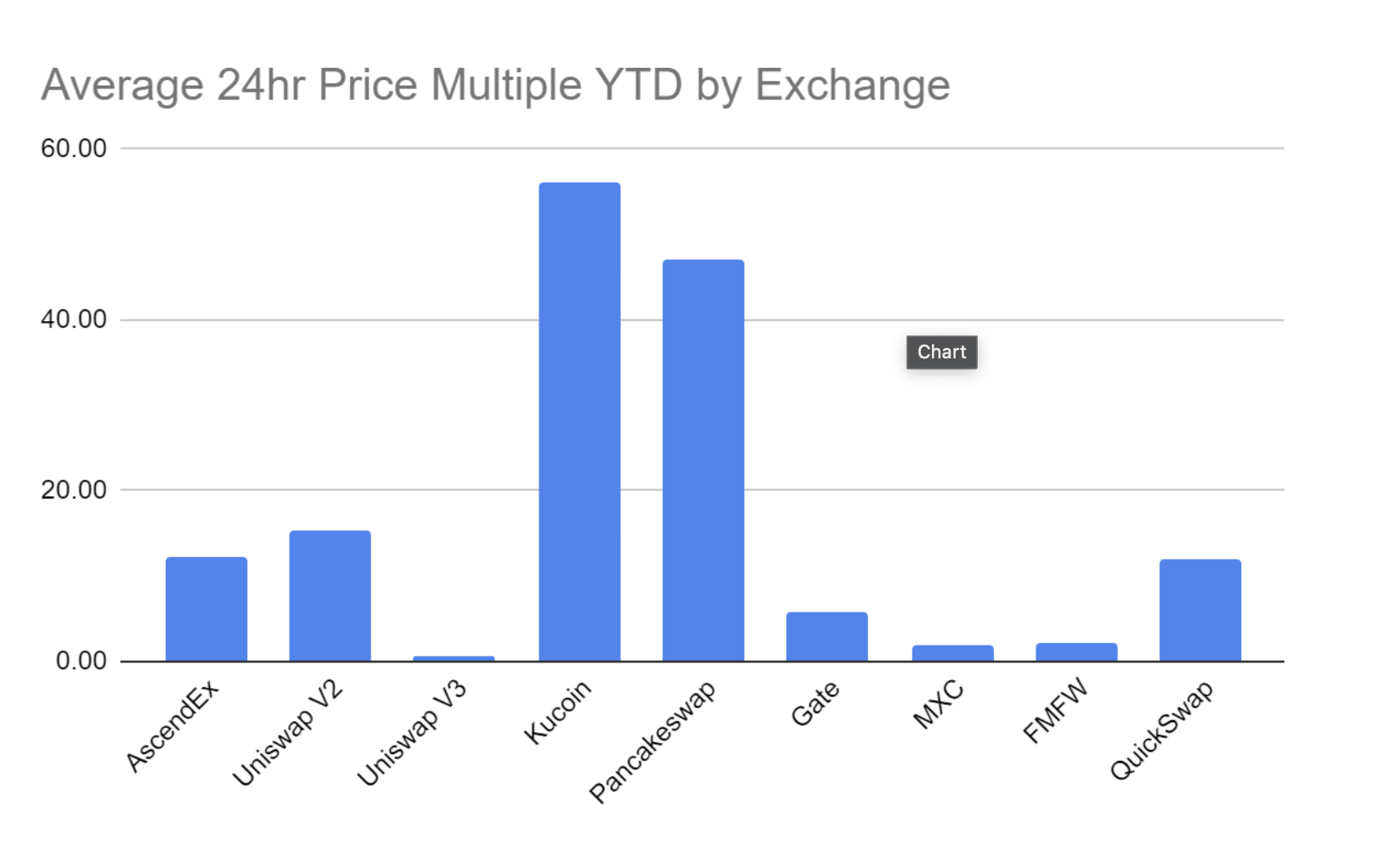

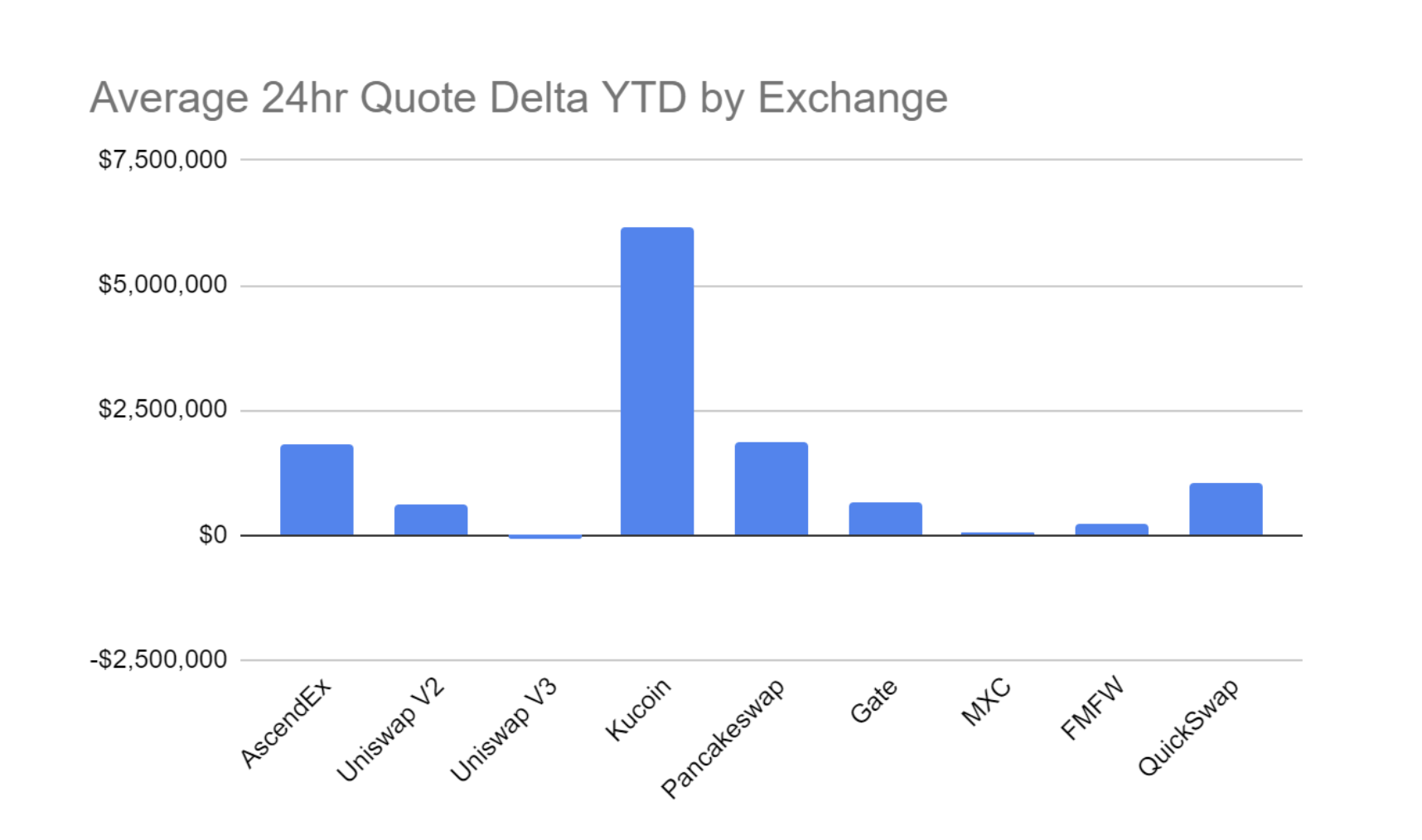

Fast forward as we close off November, we've seen the most considerable period of market frothiness eclipsing all prior periods year-to-date. For November 2021 year-to-date (YTD), Acheron launched fifty-four unique primary listings across nine exchanges.

Let's look at the numbers:

To recap what these numbers represent:

A favorable price multiple indicates demand above the opening price following market-open

An unfavorable price multiple indicates distribution below the opening price following market-open

A positive quote delta suggests traders were net buyers of tokens following market-open

A negative quote delta suggests traders were net sellers of tokens following market-open

These charts above clearly indicate the market for primary listings is in the current total exuberance "up-only" phase. Selectivity is thrown out the window, and retail buys anything and everything. As highlighted in last month's report, once the market enters up-only mode, a recessionary cycle begins looming on the horizon.

So what does that look like exactly? Let's walk through it:

There is a surge in projects rushing to market, shallow quality teams betting on market momentum to bolster the lack of fundamentals.

Exchanges are overwhelmed with activity, increasing listing fees to accommodate demand and opening new markets as quickly as possible to capitalize on bull-market pricing.

Projects are frivolously spending treasury and over fragmenting their liquidity across too many venues without considering market cycles or downside risk (easy come, easy go).

Initial market pops begin to compress as retail demand is exhausted due to market saturation.

Tokens trading at 50-100x above the post-TGE opening price with 1000% year one inflation have low basis flippers ready to judiciously liquidate following each unlock.

Capital begins to take a flight to majors and stables.

Market makers lower order sizes, reduce risk, retail LPs and projects remove liquidity from AMMs.

Panic sellers liquidate into thinner liquidity, causing rapid market deterioration.

Projects liquidate treasury tokens to shore up capital to continue as a going concern, further depressing valuations.

Token burns, restructuring of SAFT agreements, and other financial engineering to create float sinks and reduce emissions.

Period of low volatility and stagnation, followed by smart money accumulation, and a new cycle begins

As a liquidity provider, the current phase of the market becomes challenging to navigate. In general, hot markets (our current situation) require market makers to quote deeper as more traders interact with our orders. Quoting deeper liquidity requires the market maker to take more risk but a higher chance of settling any exposure. Softer markets, however, require the opposite. The market maker must reduce the capital at risk as any exposure picked up is less likely to be settled. As the conditions for primary listings are in extreme exuberance mode, we need to continue to provide deep liquidity for traders to interface with. While at the same time, we are observing our primary listings for an early indication of market saturation. At which point, we need to dial back our risk to preserve capital and ensure we can continue quoting in the face of significant change in trend.

As we roll into December, Acheron has seen an unprecedented amount of inbound deal flow, primary listings scheduled, and follow-on listings. Today alone, we executed two primary listings and three follow-on listings. While these conditions are exciting to operate in, we monitor our listings closely for the tide to turn.

You can read more about the "First-day-pop" and its utility as a potent indicator to gauge overall market health along with other market commentaries in my previous posts:

THE CONTENT ON THIS WEBSITE IS NOT FINANCIAL ADVICE

The information provided on this website is for information purposes only and does not constitute investment advice with respect to any assets, including but not being limited to, commodities and digital assets. This website and its contents are not directed to, or intended, in any way, for distribution to or use by, any person or entity resident in any country or jurisdiction where such distribution, publication, availability or use would be contrary to local laws or regulations. Certain legal restrictions or considerations may apply to you, and you are advised to consult with your legal, tax and other professional advisors prior to contracting with us.