02 Nov 2021

02 Nov 2021

Traders like CEX

Building on my previous article, Analyzing the "First-Day Pop" in Digital Asset Markets; a Market Maker's Perspective, I'd like to update our view of the current market for primary listings and where price discovery and liquidity are moving.

Before we look at the updated numbers, to recap:

- A favorable price multiple indicates demand above the opening price following market-open

- An unfavorable price multiple indicates distribution below the opening price following market-open

- A positive quote delta suggests traders were net buyers of tokens following market-open

- A negative quote delta suggests traders were net sellers of tokens following market-open

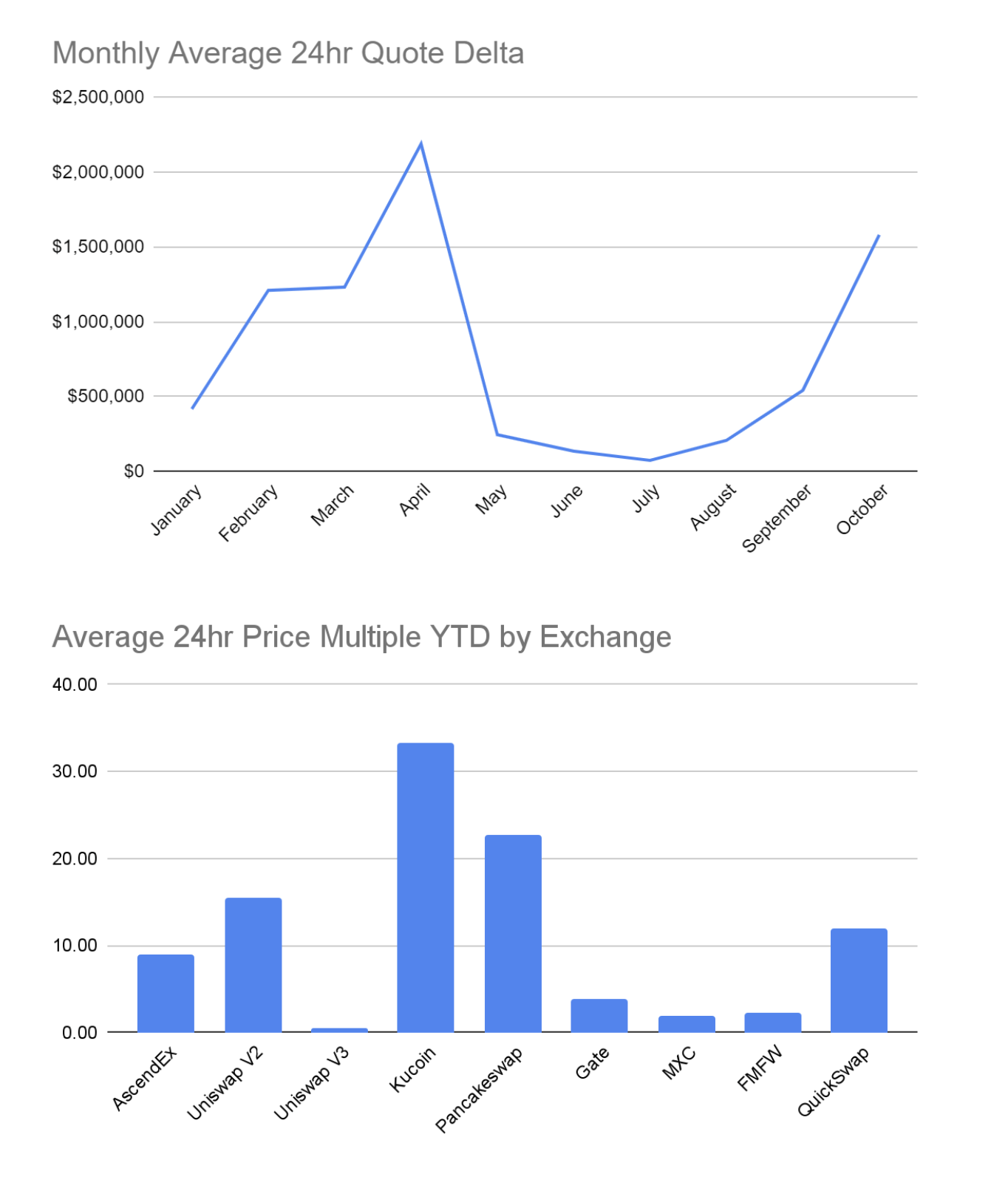

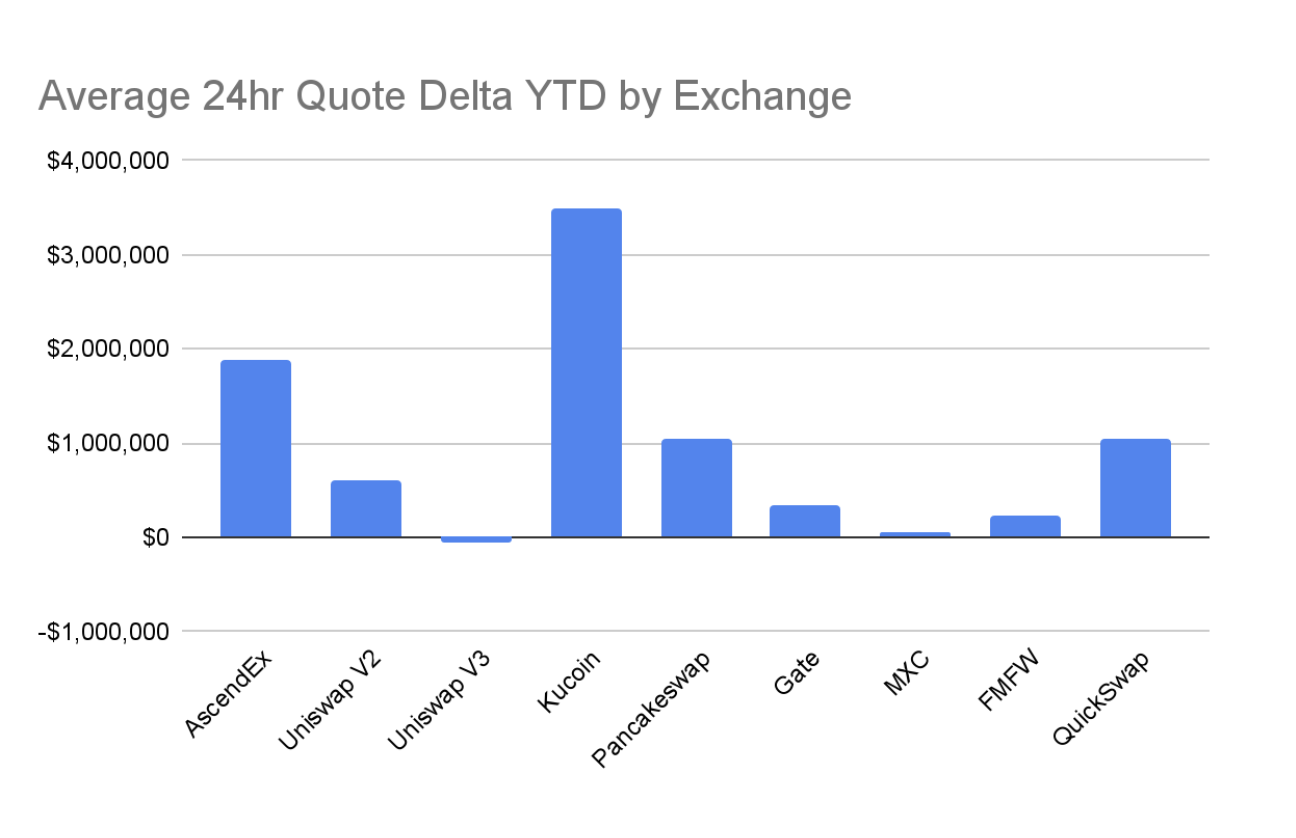

For October 2021 year-to-date (YTD), Acheron launched forty-nine unique primary listings across nine exchanges, as illustrated in the following charts:

In my last post, where we looked at data for 2021 through August, we highlighted that, on average, price multiples were higher on DEX launches, while quote deltas were higher on CEX primaries. This phenomenon indicated that CEX launches drove more efficient price discovery. In contrast, runaway price action was more prevalent on DEX launches due to sniping bots and a lack of resting sell-side liquidity.

We also concluded that, in contrast to the first quarter, where valuations were overly frothy, and the second quarter where performance was flat and in some cases negative, the conditions in the third quarter were favorable for primary listings and building positive momentum.

As we close the third quarter and are one month into the fourth quarter, it is clear that momentum has not only been building, but liquidity has been gravitating towards top-tier centralized exchanges. Particularly AscendEx and Kucoin's primary listings significantly outperformed DEX launches in 24-hour quote deltas, and Kucoin exceeded in price multiples.

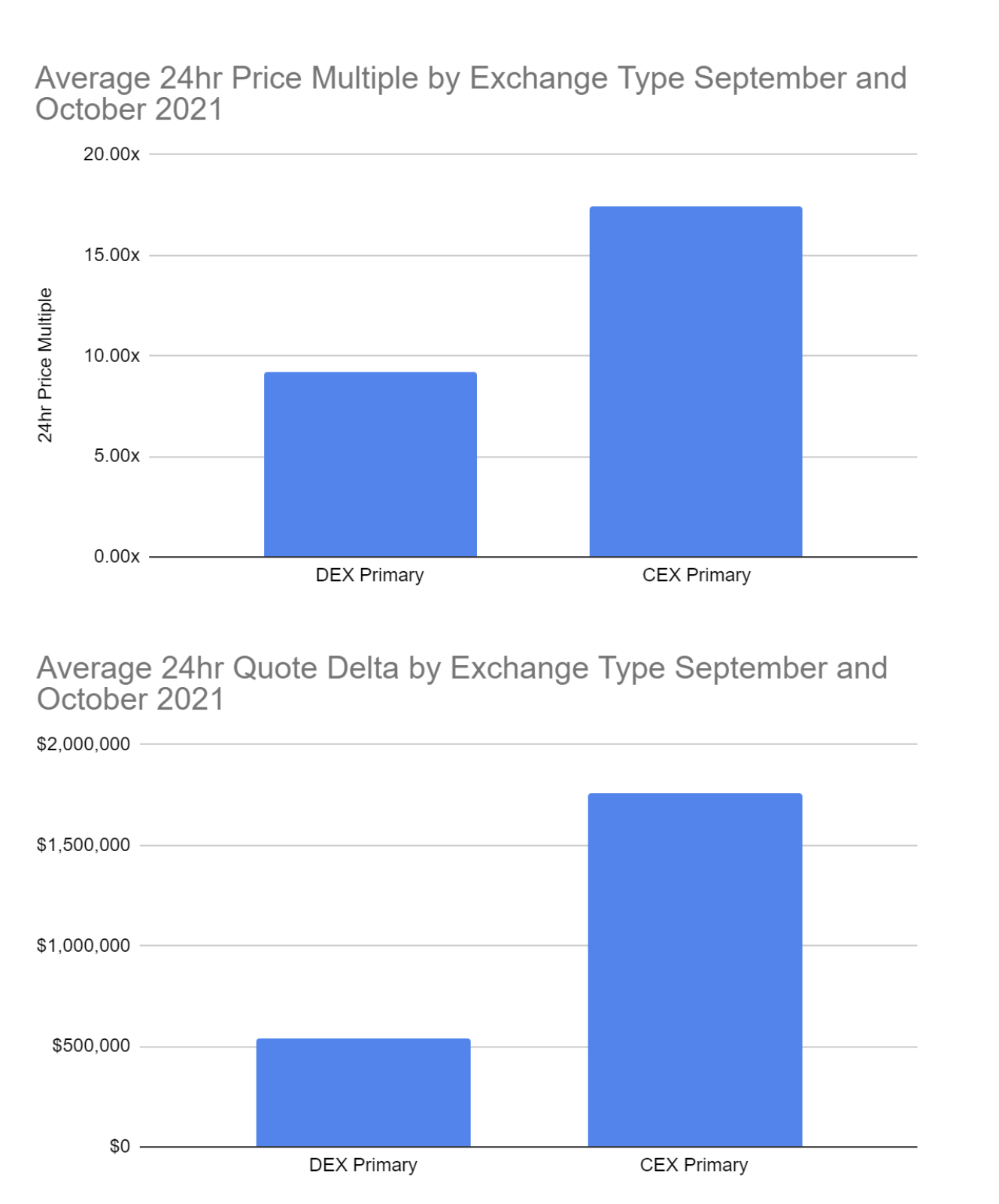

Trader preference for CEX primary listings in recent months could not be more clear considering the following charts:

We believe this is a natural evolution as liquidity seeks the most efficient venue for price discovery. DEX’s continue to provide a low-cost barrier to execute a primary listing; however, they often create significant challenges due to sniping bots, high transaction costs, and runaway price action. The end-user buys tokens at inflated prices due to sniping bots. The project sells tokens at low prices to sniping bots. High gas costs further exacerbate these challenges.

Projects have emerged in the space claiming to offer “anti-bot” products, which amount to a whitelist inserted into a project’s smart contract. The whitelist effectively renders any tokens bought outside of a predefined set of wallets at the launch unsellable. Not only does this solution prevent open price discovery as it limits the participants to only known addresses, but it also creates liability to the project as anyone who had their tokens frozen or otherwise unsellable can create a claim against the project for the losses.

To conclude, we believe that projects will seek out structuring primary listings with centralized exchanges more rigorously. In contrast, the days of allocating capital into an automated market maker or AMM-based decentralized exchange at the opening price will become a less viable option.

Furthermore, we believe DEXs will become increasingly favored as follow-on listings to expand the global liquidity footprint following initial price discovery. As a follow-on listing, the issues that plague DEX primary launches can be eliminated as the front running bounty no longer makes sense given initial price discovery has already taken place and a fair market price for the asset is readily available.

Last, as we look at the current conditions for primary listings as an indicator of overall market health, we are trending back towards exuberance territory marked by both a surge in first-day pop’s as well as significant quote deltas. However, we see more outlier performance, meaning traders are still allocating selectively among projects they perceive as the highest quality. Selectivity is an important attribute. If the market reaches total exuberance where everything is “up only,” many low-quality participants will flood the market with supply. Such events exhaust retail demand and could lead to another recessionary cycle that we saw play out earlier in the year.

THE CONTENT ON THIS WEBSITE IS NOT FINANCIAL ADVICE

The information provided on this website is for information purposes only and does not constitute investment advice with respect to any assets, including but not being limited to, commodities and digital assets. This website and its contents are not directed to, or intended, in any way, for distribution to or use by, any person or entity resident in any country or jurisdiction where such distribution, publication, availability or use would be contrary to local laws or regulations. Certain legal restrictions or considerations may apply to you, and you are advised to consult with your legal, tax and other professional advisors prior to contracting with us.