30 Aug 2021

30 Aug 2021

Analyzing the "First-Day Pop" in Digital Asset Markets; a Market Maker's Perspective

The “first-day pop” or “IPO pop” is one of the more commonly cited IPO success measures and indicators of market health in traditional securities markets. IPO pops tend to be more significant when markets are hot and lower when markets are soft. The same holds for digital asset markets following a primary listing whereby the asset becomes available for public market trading.

However, unlike in digital asset markets, investment bankers try to price an asset very close to the expected market value following public trading. Bankers try to “get it right” because any underpricing of the asset results in fewer funds that would have gone to the company going public. Bankers also do not want to overprice the asset, which would lead to a drop in Price on opening day, leaving investors disgruntled that they paid too much while concurrently hurting the stock’s future potential.

In simple terms:

Number-go-up a little = everyone happy

Number-go-up too much = company mad, investors happy

Number-go-down = everyone mad

These relationships have similar dynamics to newly tradable digital asset markets, with one key difference:

The opening price for a digital asset market is often purposefully underpriced by projects, leading to much higher first-day pops than in traditional markets.

In traditional markets, passive investors mainly hold shares, whereas, in digital asset markets, tokens are ideally held by active network participants. As such, the long-term success of a digital asset market is highly dependent on the strength of its token holders. In context, going public in securities markets is often an exit for early stakeholders; going public in digital asset markets is just the beginning. Given the importance of creating a highly incentivized token holder base, projects often default to an opening price that is the same or similar to the valuation their private investors paid, allowing the community to get in at the lowest Price possible. However, a highly favorable opening price is also why sniping bots have become so prevalent in digital markets. It pays to be first.

The result is frequently much, much higher first-day pops in digital markets compared to traditional IPOs. However, the same market-health heuristics apply: pops are higher in bull markets and lower in bear markets.

As a digital asset market maker, we hold the task of providing two-way liquidity in hyper volatile markets in the face of often highly underpriced primary listings. As a market maker, we seek to accomplish two primary objectives:

Enable market efficiency by providing adequate two-way liquidity at whatever price the market dictates while managing inventory risk;

Act as a seller of last resort mitigating exuberant, unsustainable rallies, and a buyer of last resort, mitigating market collapses.

To accomplish these objectives effectively, we carefully monitor our primary listings, which provide public and proprietary insight into the health of demand for digital assets. Specifically, we are tracking 24hr Price Multiples and 24hr Quote Deltas (the net change in our account balance) following a primary listing.

- A favorable price multiple indicates demand above the opening price following market-open

- An unfavorable price multiple indicates distribution below the opening price following market-open

- A positive quote delta suggests traders were net buyers of tokens following market-open

- A negative quote delta suggests traders were net sellers of tokens following market-open

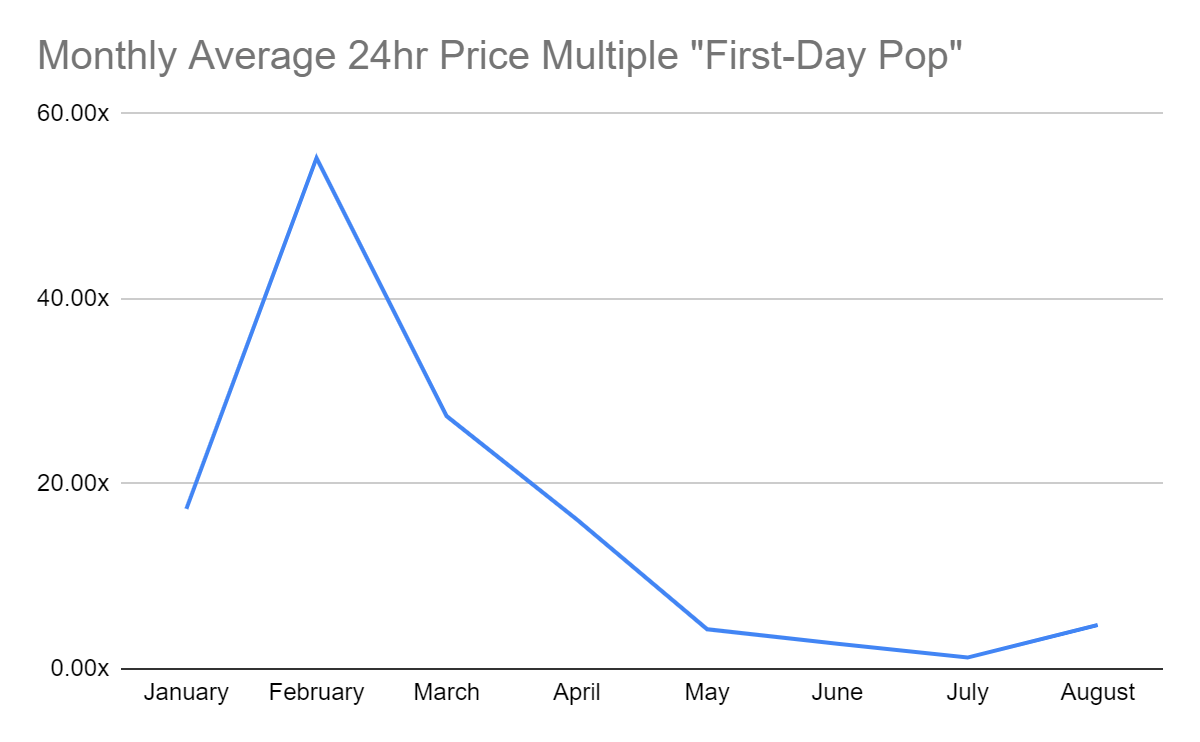

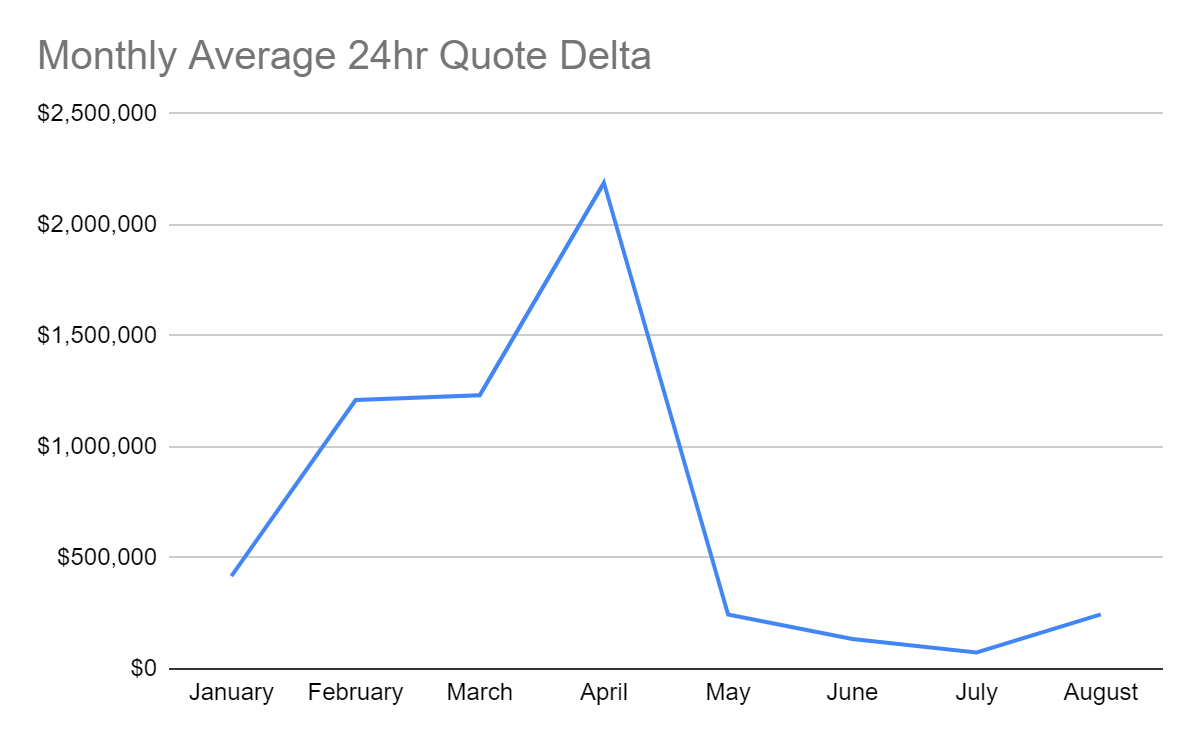

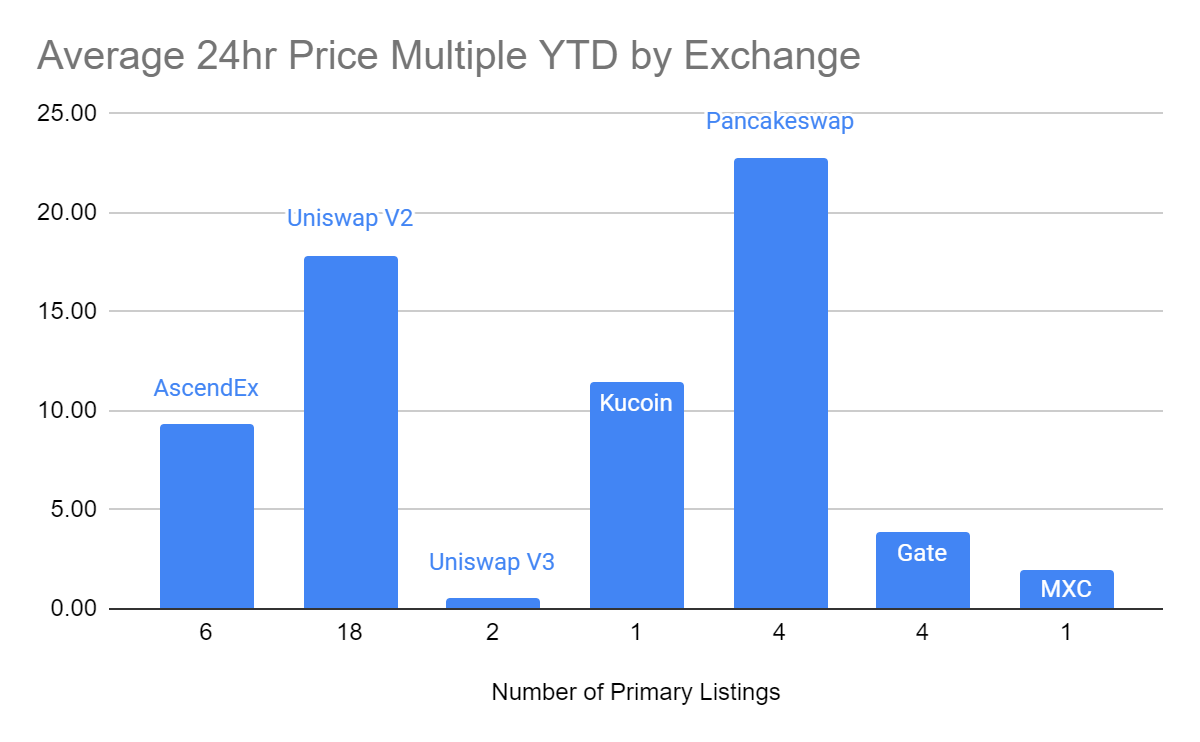

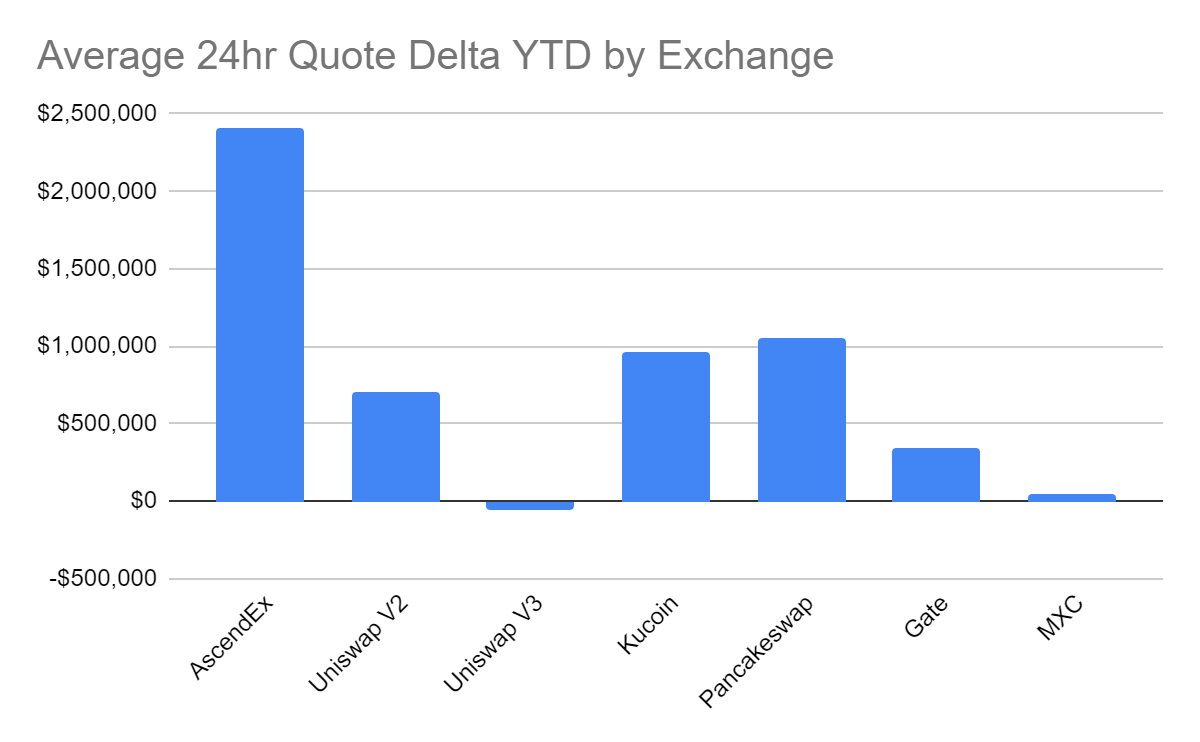

For August 2021 year-to-date (YTD), Acheron launched thirty-six unique primary listings across seven exchanges, as illustrated in the following charts:

The first quarter of 2021 yielded unprecedented retail demand for primary listings. However, rolling into April 2021, while Bitcoin and Ethereum saw fresh all-time highs, we experienced a swift change in market-open dynamics giving us an early indicator that market momentum was waning. For example, we saw the median 24hr Price Multiple drop from 21.21x in March to 8.5x in April. This level of insight is not only crucial for ensuring strategies are appropriately configured for primary listings but extends through an overarching view of inventory management across all our markets. In general, hot markets require market makers to quote deeper as more traders interact with our orders. Quoting deeper liquidity requires the market maker to take more risk but a higher chance of settling any exposure. Softer markets, however, require the opposite. The market maker must reduce the capital at risk as any exposure picked up is less likely to be settled.

An automated market maker or AMM-based decentralized exchanges yielded the most significant first-day pops. In contrast, centralized or CEX based exchanges offered the largest 24hr quote deltas with more moderate first-day pops. This dynamic indicates that CEX’s offer greater market efficiency for primary listings, while AMM-based exchanges may lead to unsustainable run-away price action. This relationship is likely driven by 1) the wide prevalence of competing sniping bots operating on AMM-based DEXs, 2) the lack of limit orders on DEX’s leading to a deficit in resting sell-side liquidity.

As we look at the current conditions, August saw a 388% increase in 24hr Price Multiple and a 331% increase in 24hr Quote Delta from July performance; however, the numbers are still dramatically reduced relative to what we experienced the first quarter. Exuberant demand for tokens is still absent, and retail is allocating selectively. Consequently, the highest quality projects may offer moderate to strong performance coupled with sensible valuations. In contrast, lower quality projects are unlikely to benefit from “a rising tide lifts all ships” dynamics that were present earlier this year.

As mentioned previously, token projects seek to attract network participants at favorable valuations — as highly incentivized active network participants create more robust networks. When first-day pops are too high, the market is typically overcrowded with speculators, drowning out the opportunity to build a solid holder base. With a 24hr Price Multiple for July clocking in at 4.75x, the current market environment is most akin to; Number-go-up a little = everyone happy. This climate is favorable for both high-quality projects and potential token network participants alike.

In conclusion, we believe that the “First-Day Pop” is a potent indicator for market makers and traders to gauge overall market health and revisit their outlook on asset performance and appetite for risk. Further, we believe it is essential to consider opening market dynamics on CEXs vs. AMM-based DEXs. Competing sniping bots and a lack of resting sell-side liquidity may create unsustainable valuations shortly following a DEX primary listing that users should observe.

THE CONTENT ON THIS WEBSITE IS NOT FINANCIAL ADVICE

The information provided on this website is for information purposes only and does not constitute investment advice with respect to any assets, including but not being limited to, commodities and digital assets. This website and its contents are not directed to, or intended, in any way, for distribution to or use by, any person or entity resident in any country or jurisdiction where such distribution, publication, availability or use would be contrary to local laws or regulations. Certain legal restrictions or considerations may apply to you, and you are advised to consult with your legal, tax and other professional advisors prior to contracting with us.