20 Dec 2023

20 Dec 2023

Case Study: Chainflip, Demystifying Effective Pre-Market Orderbook Structuring

Introduction

The initial price discovery phase for a new token is often marked by significant volatility and speculation, presenting a unique challenge in balancing supply and demand on a large, public scale. The transition from private to public markets is most commonly facilitated via a centralized exchange’s pre-market order submission.

Market makers are tasked with constructing a pre-market orderbook to facilitate a project’s entry into public markets. The primary goal of this orderbook is to provide a foundation for orderly price discovery, where prices accurately reflect the balance of supply and demand without undue volatility. The effectiveness of achieving this goal, however, is subject to variation and heavily dependent on the strategy adopted by the market maker, which may not always align with the principles of facilitating efficient price discovery. Thus, ensuring adequate liquidity is available upon market open is of supreme importance.

Scenarios & Approaches

Before we break down the differing approaches commonly taken by market makers, it is important to understand supply and demand.

There are three potential scenarios when understanding the market dynamics of premarket orders.

SUPPLY ~= DEMAND: This is the ideal scenario. Initial demand will match initial supply permitting the foundation for orderly price discovery. As a result, market makers can deploy two-sided capital to allow efficient trading of an asset at its fair market value.

SUPPLY < DEMAND: This scenario creates an environment with artificially elevated prices that do not match legitimate market dynamics. Initial demand will be greater than the initial supply resulting in new entrants buying at inflated prices prior to a swift decline in the market.

SUPPLY > DEMAND: This scenario creates an environment with artificially suppressed pricing. Initial demand will be squashed by initial supply creating a depressed trading environment

Understanding these scenarios sets the stage for understanding how market makers operate in our industry. There are four “approaches” in pre-market orderbook construction that are utilized within our industry.

Naive Approach: The market maker does not understand the importance of building a premarket orderbook to promote liquidity upon primary listing and facilitate efficient price discovery. This market maker essentially leaves the market open to the public in an illiquid manner and provides liquidity at a later point after disorderly price discovery occurs and irreparable damage has already happened. The naive approach is generally utilized by firms that trade via client’s API keys or other retainer-based models which provide no performance incentive for the market maker. Read more about types of market makers here: https://acherontrading.com/blog/fundamentals-types-of-market-makers

Parasitic Approach: The market maker intricately understands premarket orderbook submission, but willingly chooses to sit on the sidelines. This market maker waits for uninformed retail bids to stack up at inflated prices. This market maker may even manipulate the market by buying up thinly offered tokens, catalyzing “FOMO” and creating a sense of scarcity. Once peak opportunity is established, following an illiquid and inflated public market open, the parasitic market maker shorts the token, taking bids, while simultaneously placing aggressive limit sell orders to soak up demand. This market maker catalyzes a perpetual decline in the token, which further increases the realizable value of their short position. The strategy is characterized as parasitic, as it feeds off the initial demand, benefiting from detrimental effects on the health of the token market. Read more about the parasitic approach here: https://acherontrading.com/blog/reshaping-loan-call-option-strategies-for-a-healthier-token-ecosystem

Transitory Approach: Alike the parasitic strategy, the market maker understands pre market orderbook structure but overwhelmingly places sell liquidity to ensure their position is filled due to their monopolistic holding. This market maker will be heavy net sellers at most prices above market open. It is typical for this approach to be taken by a market maker looking to quickly maximize their performance fee or by a pseudo market maker aiming to close an OTC trade. This approach typically results in market abandonment as the market maker removes any potential upside.

Symbiotic Approach: The market maker intricately understands premarket orderbook submission and tactfully structures opening orderbook liquidity in favor of building long term value in the token market. The result is a relatively accurate forecast of expected demand and initial placement of liquidity to satisfy that demand via premarket orders, resulting in an initial phase of price discovery that accurately reflects the asset's market value. This permits the deployment of two sided liquidity to further orderly price discovery.

Now that we’ve discussed the approaches for placing premarket orders how can we measure their effectiveness?

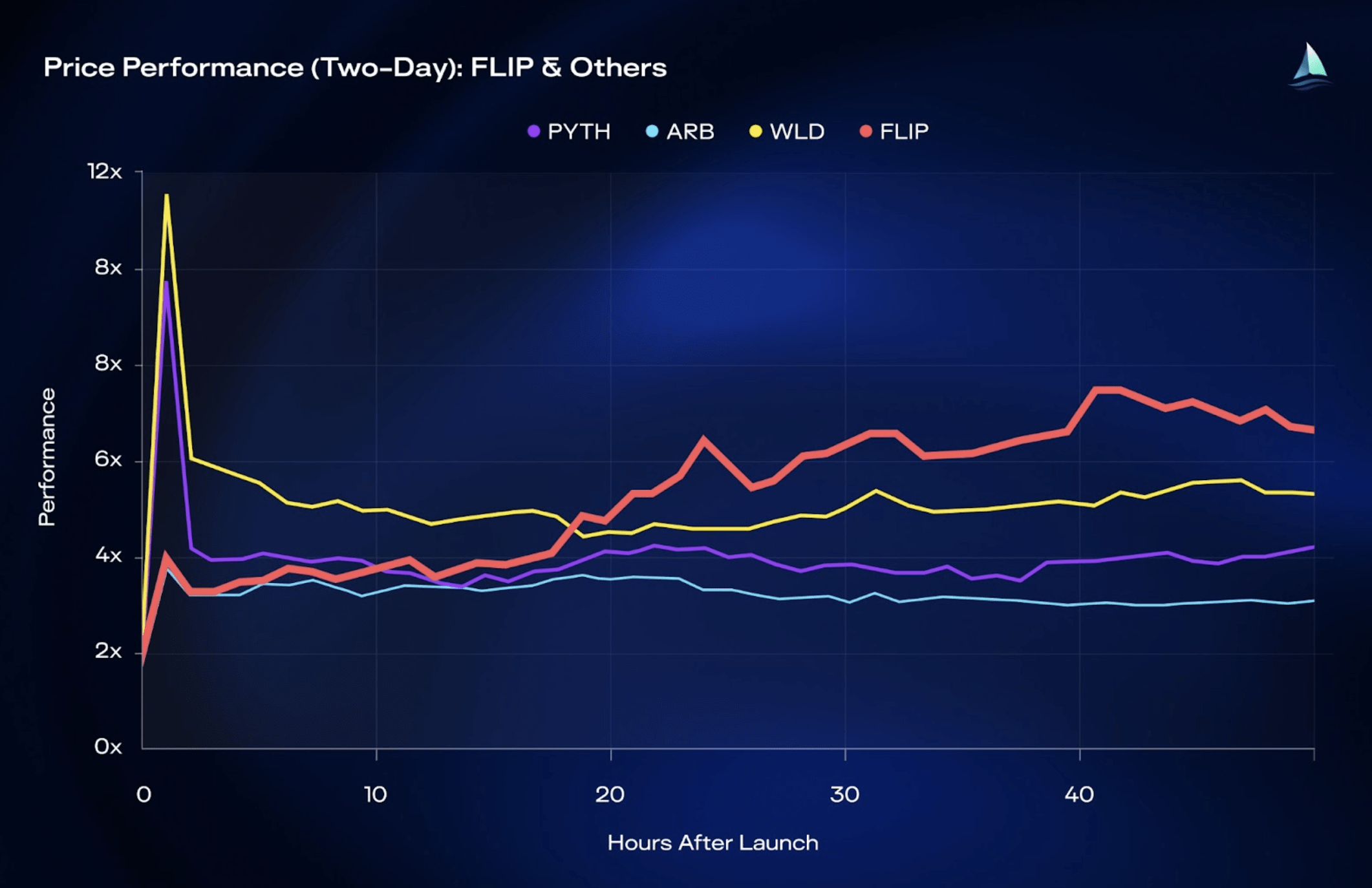

To assess the efficacy of market makers' strategies, we delve into a detailed analysis. We track the price multiple performance of tokens within two critical periods: the initial two days post-listing (analyzed hourly) and the first two weeks (analyzed daily). This data, sourced from the project's primary trading platform or reliable aggregators, undergoes normalization for comparative analysis across different projects.

Central to our analysis is the Relative Change in Volatility, or RCV, to gauge the impact of pre-market orderbook strategies on price volatility. It's calculated by the following formula.

This output quantifies the change in volatility when the ATH (All-Time High) price is considered versus when it's excluded. A higher absolute value of the RCV indicates a more significant discrepancy in volatility, pointing towards potential mismanagement of the pre market orderbook.

A positive value suggests an undersupplied orderbook, potentially indicative of a parasitic or naive market maker who fails to provide adequate liquidity pre-market.

A negative value implies an oversupplied orderbook, which might be characteristic of an overly aggressive transitory market maker or an asset priced too high.

In this case study, we contrast Chainflip's approach with similar projects, delving into their respective volatilities and the significant role of initial price discovery in establishing market stability

Case Study: Chainflip

Through the token’s initial 48 hours, FLIP’s pre-market orderbook placement was far superior to that of comparable launches, as evidenced by the comparatively minimal change in volatility when excluding the ATH data point. Specifically, FLIP's relative change in volatility is 0.07%, indicating a balanced and effective approach to managing the initial orderbook

In contrast, other launches exhibited significant changes in volatility, with increases as high as 73.99% (PYTH) and 61.83% (WLD). These figures suggest an undersupplied market where the initial ATH data point is an outlier, indicative of a market environment that is more susceptible to manipulation or influence from market makers, who might prioritize their own gains over orderly price discovery in the token’s initial period.

Extended Analysis: FLIP

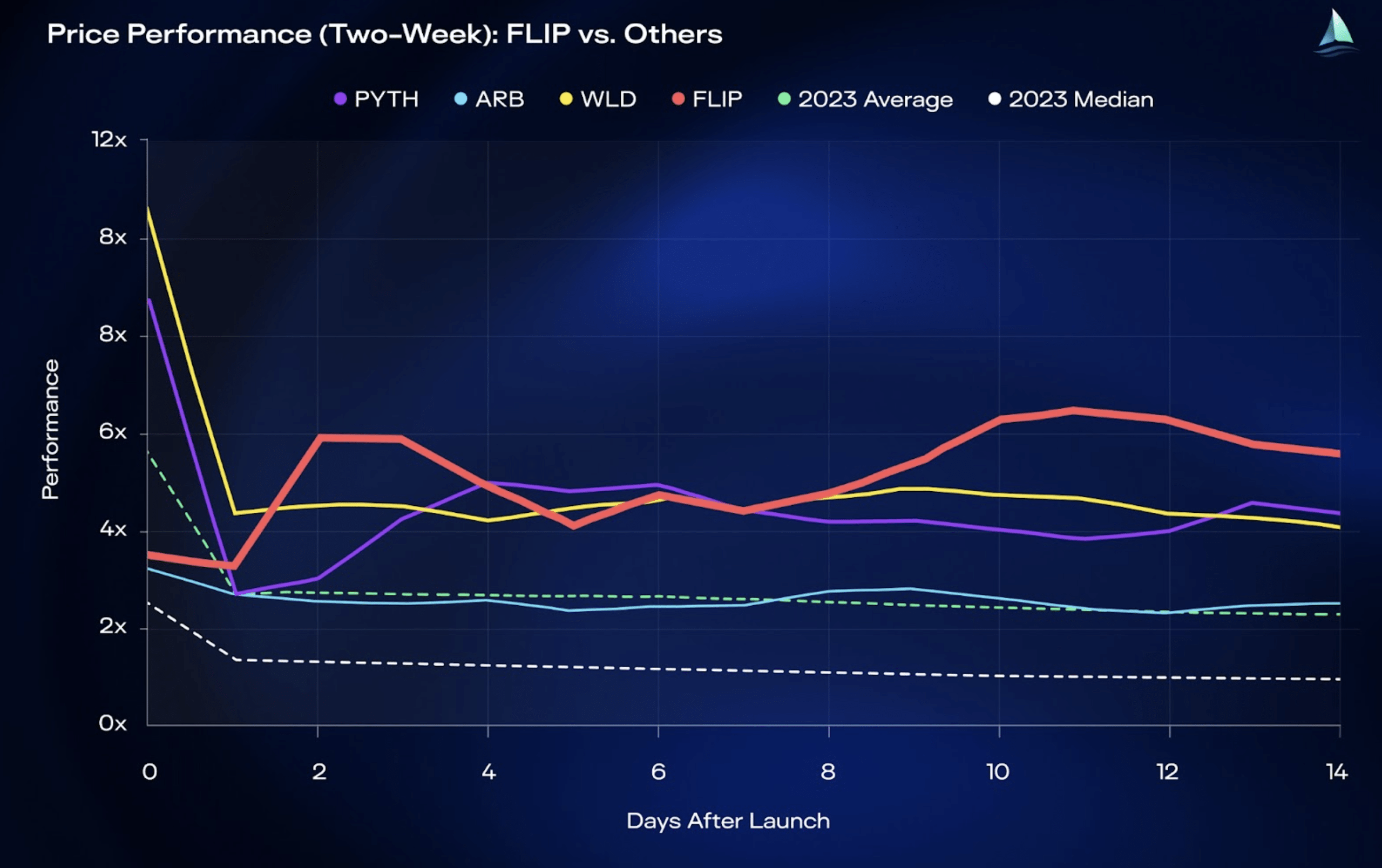

Following the initial launch period, market makers should focus on maintaining a two-sided, price-agnostic presence. This involves deploying diverse liquidity strategies across exchanges, ensuring the market’s liquidity is resilient with a high degree of uptime. We are able to test a strategy’s effectiveness as we expand our data set to 14 days.

FLIP’s relative 14-day change in volatility significantly outperforms that of its competitors, indicating a more stable and effectively managed market confirming the ATH data point aided in orderly price discovery. In contrast, the additional data points to deteriorating conditions in the WLD and ARB markets, with WLD’s performance greatly inferior.

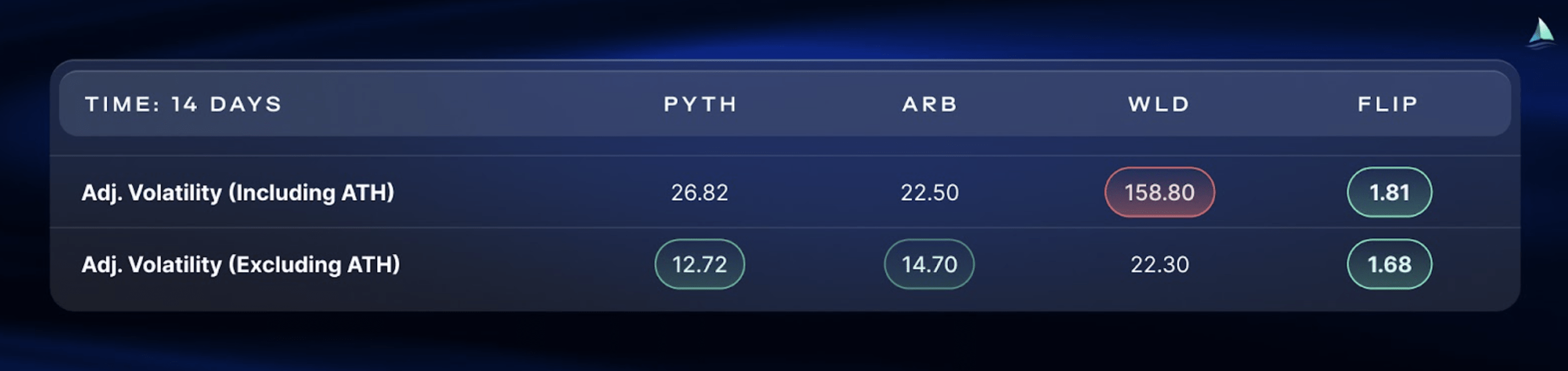

Furthermore, the difference in volatility when accounting for the token’s initial market capitalization is even more pronounced.

Considering that higher market capitalization tokens typically exhibit increased relative liquidity due to funding, larger tokens should naturally exhibit less absolute volatility. Therefore, to accurately compare volatility across differing funding amounts, we normalized volatility to neutralize the impact of market capitalization. Relative to its market cap, Chainflip recorded the lowest volatility among its peers, both including (1.81) and excluding (1.68) the initial surge. This is not just a demonstration of effective liquidity management but also highlights success in mitigating unhealthy market volatility.

FLIP's approach demonstrates a well-calibrated strategy that balances supply and demand effectively. This balance is crucial in pre-market phases, where the potential for high volatility can lead to erratic price movements and can undermine market confidence. FLIP’s strategy not only facilitated smoother price discovery but also contributed to a healthier, more sustainable market environment in the long term. This is a testament to their understanding of the intricacies of token economics and the importance of measured, strategic pre-market planning.

TLDR

This article examines market makers' strategies in structuring pre-market order books and their effectiveness at balancing supply and demand in relation to orderly price discovery.

Key Scenarios:

Supply ≈ Demand: Ideal for orderly price discovery.

Supply < Demand: Leads to artificially high prices, quick market decline.

Supply > Demand: Results in suppressed prices, depressed trading environment.

Approaches:

Naive Approach: Lack of premarket liquidity, resulting in disorderly price discovery.

Parasitic Approach: Manipulative, creating artificial scarcity and exploiting retail bids.

Transitory Approach: Overwhelming sell liquidity, leading to market abandonment.

Symbiotic Approach: Balanced liquidity for long-term orderly market conditions.

Case Study - Chainflip:

Relative Change in Volatility (RCV): Key metric to assess market stability comparing initial price pop to subsequent price action.

FLIP's Performance:

RCV of 0.07% in the initial 48 hours, indicating a balanced approach.

Outperforms peers (PYTH at 73.99% RCV, WLD at 61.83% RCV) in liquidity management.

Extended Analysis: 14-day volatility data confirms stable, effective market management for FLIP while others struggled.

Findings:

Adequate pre market forecasting and modeling helps ensure a smooth transition from public to private markets via a centralized exchange’s pre market orderbook.

Here, a token will undergo the tests of public markets and begin the process of price discovery.

Without sufficient planning, a project may be faced with unprecedented problems due to parasitic, naive, or transient market makers who aim to maximize their own position rather than promote sustainable liquidity.

Through thorough analysis we shed light on the immediate impact of pre-market orderbook structuring but also offer a longer-term view of the market maker's effectiveness in promoting orderly price discovery.

By examining these metrics, we can better understand the implications of different market-making strategies, ranging from naive to parasitic, and how they ultimately shape the market dynamics of newly listed tokens.

THE CONTENT ON THIS WEBSITE IS NOT FINANCIAL ADVICE

The information provided on this website is for information purposes only and does not constitute investment advice with respect to any assets, including but not being limited to, commodities and digital assets. This website and its contents are not directed to, or intended, in any way, for distribution to or use by, any person or entity resident in any country or jurisdiction where such distribution, publication, availability or use would be contrary to local laws or regulations. Certain legal restrictions or considerations may apply to you, and you are advised to consult with your legal, tax and other professional advisors prior to contracting with us.