09 Dec 2025

09 Dec 2025

Uniswap v4 and the Future of Liquidity Provision: A Market Maker’s Perspective

What is the Uniswap Protocol

The Uniswap protocol is a peer-to-peer system built on the Ethereum blockchain for exchanging cryptocurrencies. It leverages ERC-20 tokens, the Ethereum standard fungible token on the Ethereum chain.

Uniswap behaves as an Automated Market Maker (AMM) wherein traditional order book bid/asks are replaced by liquidity pools of asset pairs. As these assets are traded, their relative prices shift, and a new market equilibrium is found. Both buyers and sellers interact directly with the liquidity pool instead of with each other in an order book.

This report focuses on the latest evolution of the Uniswap Protocol, v4. The v4 evolution redesigns the Uniswap Protocol, providing developer customization over liquidity pools via hooks, and improves efficiency by moving to the ERC-6906 token standard.

The Uniswap Timeline

Uniswap v1 was released in November 2018 at Devcon 4 as the first AMM supported by the Ethereum foundation. Adoption was slow, with only $30,000 worth of deposits occurring in the first 24 hours. The AMM used a simple constant product model:

Where k is constant term defined at pool initiation, and x, y being the two assets in the pair. In v1 all pools were routed between ETH and an ERC-20 token meaning for any token pair [ERC-20, ERC-20], the transaction would first need to go to ETH.

This is the foundation of Uniswap and allowed users to quickly swap tokens outside of centralized exchanges.

In May of 2020 v2 was released. The main change v2 offered from v1 was multiple token-pair trading. Multiple token-pairs means users can swap between two different ERC-20 tokens instead of first via ETH. Uniswap v2 was much more flexible than v1 leading to a growing userbase and consolidating Uniswap as a key piece in decentralized trading.

Following the launch of v2, the September 2020, UNI (Uniswap's own token) airdrop would become a defining moment for DeFi. The airdrop rewarded early users of the Uniswap platform, retroactively distributing tokens to users. The airdrop played a crucial role in strengthening the Uniswap community which had struggled following a Uniswap fork created SushiSwap, siphoning billions of dollars of liquidity away . Distributing UNI tokens was a way of building trust and giving a sense of shared ownership in the decentralized space.

Following the airdrop, there was a surge in new Uniswap accounts being made, boosting adoption, trading volume and liquidity. Granting new governance rights to users solidified the position of Uniswap as a leader in DeFi.

This airdrop is now looked back upon as a revolutionary drop due to the scale, timing and governance it offered. 250,000 wallets claimed the airdrop, with the initial value of UNI being $3, meaning users would receive a value upwards of $1200. The drop popularized retroactive distribution models and inspired many future projects.

In May 2021 v3 launched, bringing with it concentrated liquidity allowing users to define price ranges within trading pairs, reducing arbitrage opportunities and increasing fees received. The fees in v3 were also split into three tiers allowing the user to balance fees and risk appetite.

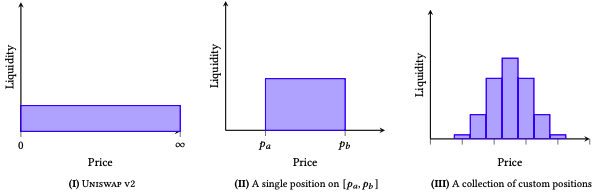

As shown in the Uniswap v3 whitepaper, liquidity can now be allocated across multiple price ranges; single (0,∞) range, a single (lower, upper) bound or a collection of custom (lower,upper) bounds.

Evolving from the constant product model, the AMM now considers the amount of liquidity provided as the value of L, equal to the square-root of k. The curve represents the real reserves of the position as denoted by:

With pa, pb defining the bounds of the range, x,y the assets and L the liquidity provided.

Uniswap v3 was adopted quickly following v2 with trading volume within the first 24 hours doubling the trading volume of the month following v2’s launch. Looking at the fees generated on v3, we saw that it took until the middle of 2021 for v3 to surpass v2 while liquidity and volume was being established.

Uniswap continued to lead the DeFi space with the launch of UniswapX. This introduced a permissionless, auction-based trading layer into Uniswap. UniswapX improved price discovery, reduced gas costs and protected users from Maximal Extractable Value (MEV) exploits, by aggregating both on-and-off-chain liquidity. It positioned Uniswap as a flexible and scalable infrastructure for the next generation of decentralized exchanges.

This brings us to Uniswap v4, the current evolution of the Uniswap Protocol. v4 introduces customizable hooks, ERC-6909 token compatibility and continuous clearing auctions (CCA), Uniswap v4 launched with strong interest from the community on January 30, 2025. As of September 2025 Uniswap v4 handles approximately $700 Million in daily trading volume. At the time of writing, Uniswap v4 on Ethereum has a ~$186 Million 24hr trading volume vs the ~$427 Million on v3. The adoption of v4 is expected to be gradual due to the complexity of hooks, large liquidity projects needing migration from v3 and recent scares such as the hack of Bunni.

Uniswap continues to expand its platform support for broader DeFi innovation with the launch of Unichain in 2025. Unichain is a Layer-2 using the OP Stack (Optimistic Rollup) on Ethereum. It was built to be a superchain, delivering fast, cheaper transactions across chains and enabling seamless multi-chain swaps. The creation of its own execution layer allows Uniswap to challenge the dominance of Ethereum L1 reliance for DeFi applications.

Uniswap v4, with Unichain and UniswapX have given Uniswap a strong platform to lead the next step of DeFi growth, with its long-term vision backed by the Unification proposal which aims to buy back and burn UNI tokens, while merging Uniswap Labs and Foundation.

What do the Changes in Uniswap v4 mean?

Efficiency

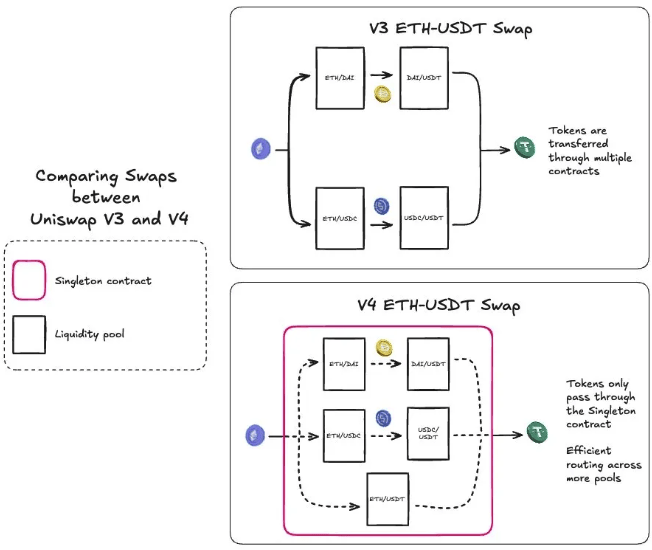

Liquidity providers and users (swappers) can leverage the new Flash Accounting System (FAS) which improves gas efficiency greatly by streamlining token transfers. The FAS is part of the new PoolManager, the core development for the Singleton contract architecture.

The singleton contract architecture has been implemented with native ETH support and adopting the ERC-6909 token standard for internal accounting. Liquidity provisioning and trading on v4 will be cheaper and more capital efficient.

The ERC-6909 internal accounting standard tokens represent user balances for multiple tokens within the contract (i.e. ETH, TokenABC, TokenEFG). ERC-6909 tokens are burnt or minted in a transaction instead of transferring in and out of the pool during transactions. The singleton contract is a single smart contract that manages all liquidity pools. In v1 to v3 an individual, separate contract was deployed for each new pool which was a gas intensive process. In v4 this is replaced with the Pool Manager. The Pool Manager holds the state for each pool within the same contract, reducing gas costs by upto 99% when making a new pool compared with v3. This is also a simpler operation in cross pool transaction as each pool exists in one address. The new architecture is more efficient and easier to deploy on new chains.

Adopting native ETH means swappers can swap to ETH directly, cutting out the need for an additional step in/out of wrapped-ETH (WETH). This directly reduces gas costs by 15% per swap, increasing capital usage efficiency.

The image below (courtesy of DWFLabs) highlights the structural changes of a LP swap using the Singleton Contract.

Continuous Clearing Auctions (CCA)

Another new addition to v4 is the Continuous Clearing Auctions (CCA) protocol. The CCA is a mechanism allowing for fairer price discovery and liquidity bootstrapping by virtue of a permissionless auction. CCA was developed alongside Aztec Network who are an Ethereum Layer-2 with a focus on privacy. Aztec will be the first project to launch on CCA in early December 2025. In a CCA launch all bidding and price discovery occurs on-chain with a smart contract to execute pricing, bidding and settlement. This ensures an open and fair auction process for all participants. In principle, by leveraging an on-chain (block to block gradual) auction, early bidding is incentivized and the price should converge to a fair market value and be less volatile to large last minute moves. Upon completion of the auction the raised tokens (and unsold) will automatically be used to create a v4 pool ensuring the project has deep liquidity from TGE.

Hooks

A hook is a smart contract a developer can “plug” into a v4 Liquidity Pool to execute custom trading logic. A hook’s logic can be implemented and executed at various points in the lifecycle of a liquidity pool, triggering on events such as initialization, large deposits/withdrawals of liquidity or swaps. In total this is 8 events that can lead to a hook callback. Instead of the liquidity pool being on a defined pricing curve, the implementation of hooks allow developers to build pools that have custom market making rules. These include dynamic fees, limit orders, time weighted average market making and custom oracle checks. Implementing hooks enable features such as volatility-adjusted fees, MEV redistribution, and more sophisticated market-making strategies. Hooks have allowed Uniswap to become a platform where new features are deployed as hooks instead of requiring the liquidity pool for each protocol update.

Experimentation with v4 hooks has been rapid in 2025, with 2500 hook enabled pools being created by time of writing, demonstrating the strength of this mechanism. Below is a key diagram outlining the process of a swap with hooks.

Below we see the workflow of a swap contract being executed with hooks. First the swap is initiated. Then a check is performed to see if there is a pre-swap hook. If yes, it executes. The same follows for the post-swap hook.

Current hook implementations include dynamic fee adjustment by using hooks to change the fees in a LP based on either market volatility or pool conditions (i.e. increase spreads in high volatility periods) and threshold encryption, as used in Angstrom’s MEV-Resistant Architecture.

The implementation of hooks can also be used to mitigate the ever-present problem of Impermanent Loss (IL). Rebalancing hooks can automatically reposition liquidity, hedging hooks can execute offsetting positions in perpetuals and MEV capture. MEV capture, as seen in Bunni’s project, captures arbitrage opportunities and sends the profit back into the pool to recover IL.

Uniswap v4 Adoption

Users are migrating to v4 with a TVL of over $1 Billion USD as of mid 2025, a milestone v4 has reached faster than v3. However users remain cautious to move liquidity tied into existing projects while the new dynamics are learned. Uniswap has provided a simple interface to migrate v3 pools to v4 and is investing heavily into security and tackling any bugs in the code. Users who find critical bugs and errors in the code are rewarded with bounties up to $15.5 million in value.

It is clear that future evolution and innovation will occur on v4, but users remain cautious until the new protocol is fully understood. It is expected that v3 and v4 will live together in the uniswap ecosystem for an extended period until blue-chip projects migrate to v4 and the momentum of adoption follows. The involvement of well known DeFi actors is a bullish sign for the viability of v4 but it remains a question of risk and reward with the recent hack of Bunni via a hook exploit serving as a stark reminder to be cautious.

Early Adoption Case Studies

Aztec Network

The Aztec Network is the first project to utilize CCA for its token launch with 1,547,000,000 tokens available for auction at a price of $0.0338. These tokens will have a vesting period of 90 days with an unlock vote available via the Aztec governance process. Should the vote not succeed there is a 12 month backstop for unlocks. This project has received $171.4 million in fundraising so far from funding rounds and public sale, including investors from Andreesen-Horowitz and Paradigm. The network already has numerous projects such as ZKPassport connecting real world ID to the blockchain and human.tech, a privacy focussed Ethereum to Aztec bridge.

The team behind Aztec quotes “CCA redefines fair access in the crypto space…” highlighting this project's intention to be the first of many to launch tokens on CCA.

Bunni

Bunni was one of the flagship projects on v4. It was designed to maximize liquidity providers' capital efficiency. This was done by introducing liquidity management strategies ontop of v4 using hooks. The “Bunni layer” addresses many of the issues in Uniswap v3 by automatically rebalancing pools by reshaping liquidity over evolving price ranges. It can also capture MEV and return it to the pool which boosts the LP yields. Bunni grew a large volume with high fee earnings highlighting how leveraging hooks was effective at maintaining tight liquidity spreads around price comparatively to static positions. However a hack lost Bunni $8.3 million by exploiting a weakness in accounting hook logic (precision/rounding error). This underscores the importance of strong audits, rigorous testing, and robust security practices, and remains a key limitation for v4’s adoption.

Silo Finance

Hooks are also leveraged by Silo Finance in a project focussed on using the v4 AMM to create isolated lending markets (Silo’s). The typical LP pools many assets which means users face systemic risk. Silo instead creates separated pools for each asset, isolating risk. To ensure each pool has enough liquidity the v4 hooks are used that implements lending logic such as interest rates, liquidations and collateral variables to the pools. This creates a synthetic lending functionality of an AMM and a money market (by the hook) in the pool. Liquidations to one pool/asset are self contained and will not affect other pools.

Silo is another key example of the dynamic use cases of Uniswap v4 hooks to create new services for users.

Concluding Remarks

Uniswap v4 represents a major leap forward for Decentralized Exchanges, offering new flexibility, privacy and efficiency. Hooks, CCA and native ETH give developers freedom and efficiency to create new services to the wider ecosystem and innovate on Uniswap’s core protocol itself. Adoption may take some time, but we expect that Uniswap v4 will solidify itself as an industry leader in the near future and remain the centre of DeFi development in ever evolving crypto markets.

References

Uniswap v3 Whitepaper, Adams, H., Zinsmeister, N., Robinson, D., & Salem, M. (2021). Uniswap v3 Core. Uniswap Labs.

Available at: https://app.uniswap.org/whitepaper-v3.pdfUniswapX Whitepaper: A Non-Custodial Dutch Auction Trading Protocol. Uniswap Labs. Adams, Hayden, Noah Zinsmeister, Emily Williams, Mark Toda, Xin Wan, et al. (2023). Available at: https://app.uniswap.org/whitepaper-uniswapx.pdf

What is Unichain? A Deep Dive into the Superchain L2 for DeFi. Nansen Blog. Available at: https://www.nansen.ai/post/what-is-unichain

Uniswap v4 Whitepaper, Adams, H., et al. (2024). Uniswap v4 Core. Uniswap Labs.

Available at: https://app.uniswap.org/whitepaper-v4.pdDWF Labs, DWF Labs. (2024, September 24). What’s New in Uniswap V4: 3 Key Changes and 2 New Protocols (updated August 25, 2025). DWF Labs Research.

Available at: https://www.dwf-labs.com/research/457-what-s-new-in-uniswap-v4-three-key-changes-and-two-new-protocolsBunni, https://bunni.pro/

Silo Finance, https://silo.finance/

Aztec Labs, https://aztec.network/

THE CONTENT ON THIS WEBSITE IS NOT FINANCIAL ADVICE

The information provided on this website is for information purposes only and does not constitute investment advice with respect to any assets, including but not being limited to, commodities and digital assets. This website and its contents are not directed to, or intended, in any way, for distribution to or use by, any person or entity resident in any country or jurisdiction where such distribution, publication, availability or use would be contrary to local laws or regulations. Certain legal restrictions or considerations may apply to you, and you are advised to consult with your legal, tax and other professional advisors prior to contracting with us.