12 Mar 2026

12 Mar 2026

Real-World Asset Tokenization - The Convergence of TradFi & DeFi

What Are Real-World Tokenized Assets?

Real world assets or RWAs are tokenized representations of traditional physical and financial assets, such as government bonds, commodities and real estate. These assets are represented as a digital token on a blockchain, with each token representing an enforceable legal claim on the underlying asset. Tokens are held and settled via distributed-ledger-technology instead of traditional intermediaries. This allows for fractional ownership, 24/7 markets and near instant settlements, allowing private retail investors access to historically institutionalized products. An asset represented on the blockchain ensures an immutable record of ownership to enforce a claim to the underlying real world asset.

Why 2026 Represents an Inflection Point for Tokenized Assets

Moving into 2026, tokenized assets have become a real investment option for many private and institutional investors, evolving from merely a speculative thesis. Since 2020 the RWAs market has grown by an estimated 2000%+ measured by market capitalization (excluding stablecoins). This growth has escaped the cyclical volatility we usually expect in the crypto market, showing that RWAs are not just a speculative bubble, but here to stay.

Macroeconomic Factors, Legislative Clarity and Institutional Capital movement are increasingly rotating idle capital on-chain into tokenized assets, as holding non-yield bearing digital assets in stablecoins is no longer economically rational.

The macroeconomic foundation of RWA growth can be clearly derived from the ending of zero-interest-rate policies (ZIRP) by global central banks. With the risk-free-rate (3mo US T-Bills) non zero it is non-optimal to hold capital in non-yielding digital assets. Through previous crypto cycles such as 2020-2021, this rate was near zero and USDT and USDC stablecoins were able to function as stores of wealth. In the current market, holding billions of dollars in stablecoins, when the risk-free-rate yields ~3-5% is a financial liability.

This macroeconomic push has led to the “Great Convergence of Traditional Finance and Decentralized Finance” as capital rotates into tokenized treasury and money market funds.

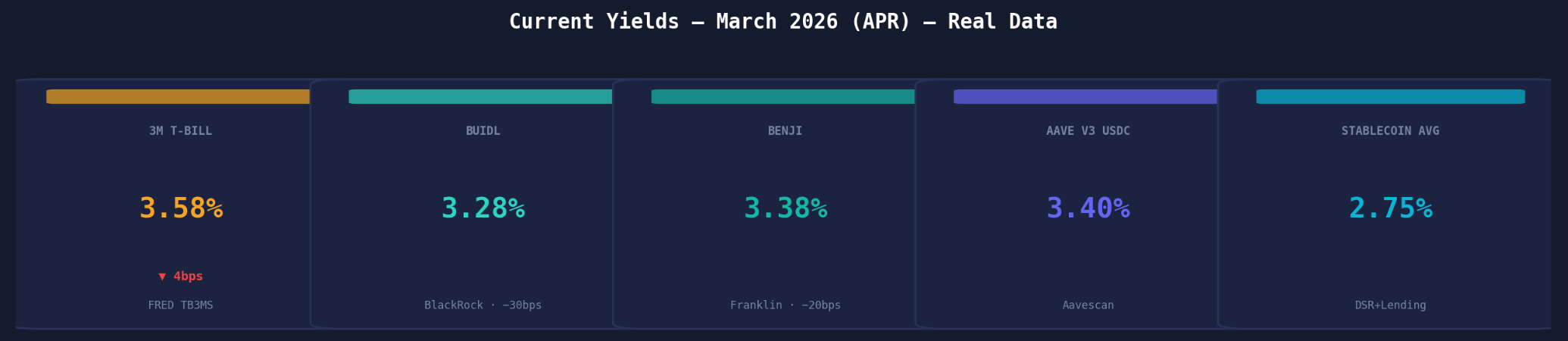

Figure 1: The Current Yields (March 2026) of [3M T-Bill (FRED), BUIDL (Blackrock -30bps), BENJI (Franklin Templeton -20bps), Aave V3 USDC (Aavescan), Stablecoin Avg (DSR + Lending Blend)]

As a MiCA-regulated market maker we are in the front seat of the structural convergence of traditional finance (TradFi) and decentralized finance (DeFi). RWAs remain a strong theme in todays market. The increased tokenization of financial assets, rewriting how ownership is recorded and transferred offers a great opportunity as institutional capital migrates on chain, a movement we see strengthening towards the end of the decade.

The Regulatory Foundations of Structural Migration

Between 2024 and 2026 the crypto industry has undergone a regulatory transformation. As the market matures and institutions become increasingly involved, a clear regulatory landscape is imperative for organic growth and capital rotation on-chain. Both Europe and The United States have codified a clear, enforceable regulatory framework.

European Regulation: MiCA

The EU’s Markets in Crypto-Assets Regulation (MiCA) has been enforceable since the end of 2024, as the world's most comprehensive regulatory framework for digital assets. This framework prohibits stablecoin issuers from paying yield to holders. This directly caused a flight of capital from stablecoins to tokenized Money Market Funds and sovereign debt (treasuries). These asset classes are currently still regulated as securities meaning yield is easily available to investors. This change has seen stablecoins become the key force for fast settlement and tokenized assets capture yield-seeking institutional capital.

Rigorous oversight, strict enforcement and audit requirements on smart contracts have added regulatory legitimacy to the market that increasingly draws institutional investors to the European market.

U.S. Regulation: GENIUS and CLARITY

In July of 2025, the United States passed the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins). GENIUS provided regulatory clarity on the federal level that mandated stablecoins be backed 1:1 by high-quality liquid assets and also banned stablecoin yields. This move mirrored the market impacts of MiCA in Europe.

The CLARITY Act, which has not yet passed into law (Passed the House in July 2025), aims to categorize tokens as digital commodities, investment contracts or payment stablecoins, allowing large institutions to invest in these markets without the legal risk of what regulation their assets would fall under. Resultingly we expect to see pension funds, insurers and large firms to enter the space and onboard onto blockchain rails.

Strong regulations across the U.S. and EU aim to converge global regulation, providing confidence and stability for market participants. Stablecoins will remain high-frequency settlement tools and RWAs will provide yield for investors seeking to gain digital asset exposure.

The Convergence of Yield - TradFi & DeFi Alignment

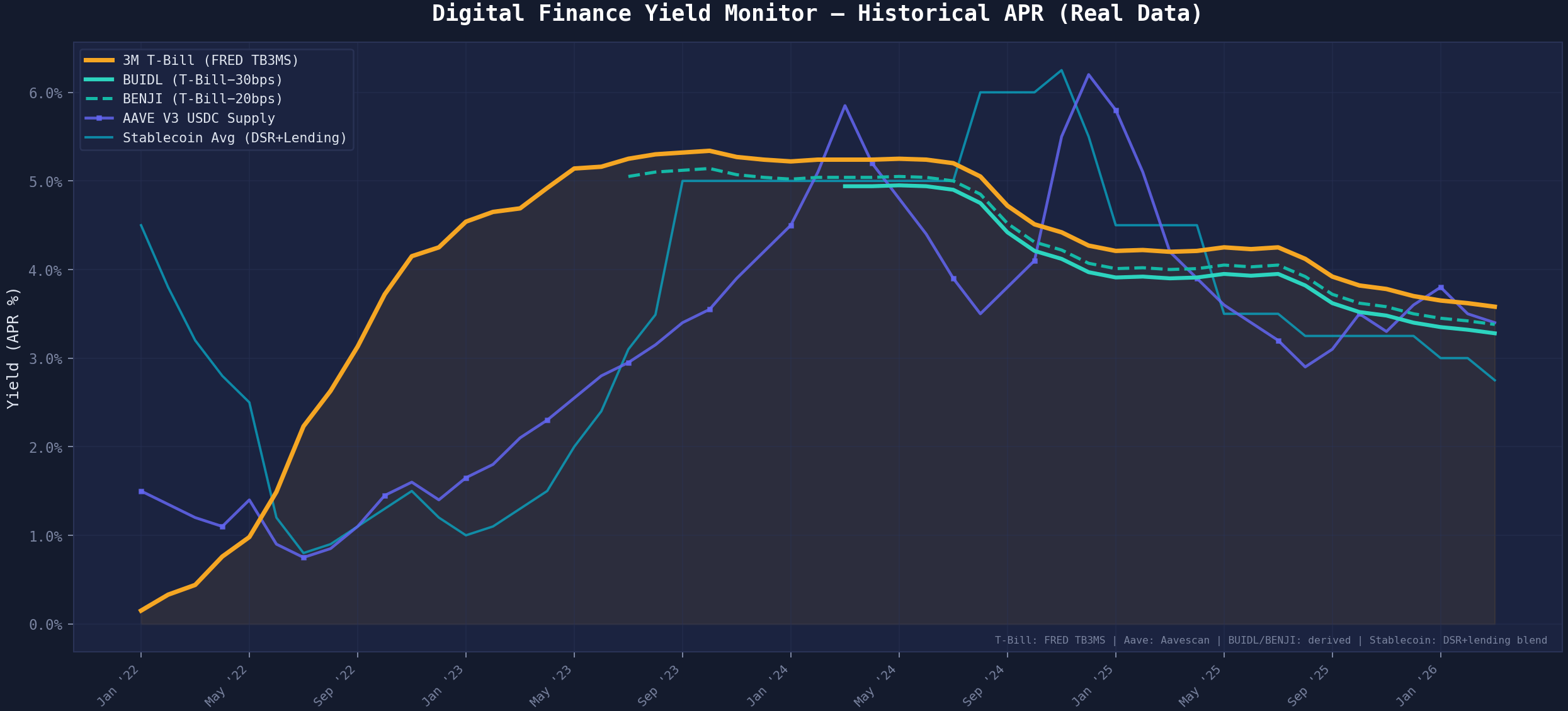

As tokenized treasuries continue to grow, the crypto industry is getting its first “DeFi risk-free-rate”. U.S. Tokenized Treasuries anchor this risk-free-rate with the chart below highlighting this convergence. (Note yields are assumed to be ex-spread-fees)

We observe that in early 2022, which was a DeFi dominant era, Aave supply rates yielded ~1.5%, while T-Bills returned 0.15%. This marked a clear disconnect between DeFi yields and traditional treasuries. Late 2020 saw a surge in treasury rates as the DeFi-TradFi spread inverted. As of 2023-2024, tokenized treasury products imported the treasury rates onto the blockchain, with BlackRock’s BUIDL and Franklin Templeton’s BENJI tokenized treasury products converged to the 3mo T-Bill, providing a key investment indicator for digital capital deployment.

Figure 2: The Historical APR of Yields, [3M T-Bill (FRED), BUIDL /BENJI (minus fee spread), Aave V3 USDC (Aavescan), Stablecoin Avg (DSR + Lending Blend)]

In the current state of the market we see the strength of this convergence. A 3-month T-Bill yields 3.58% with BUIDL and BENJI yielding 3.28% and 2.28% respectively. Aave V3 USDC supply rates yield 3.42% reflecting the demand for a leveraged digital strategy. We can also observe that stablecoin yields are remaining structurally suppressed in line with GENIUS and MiCA.

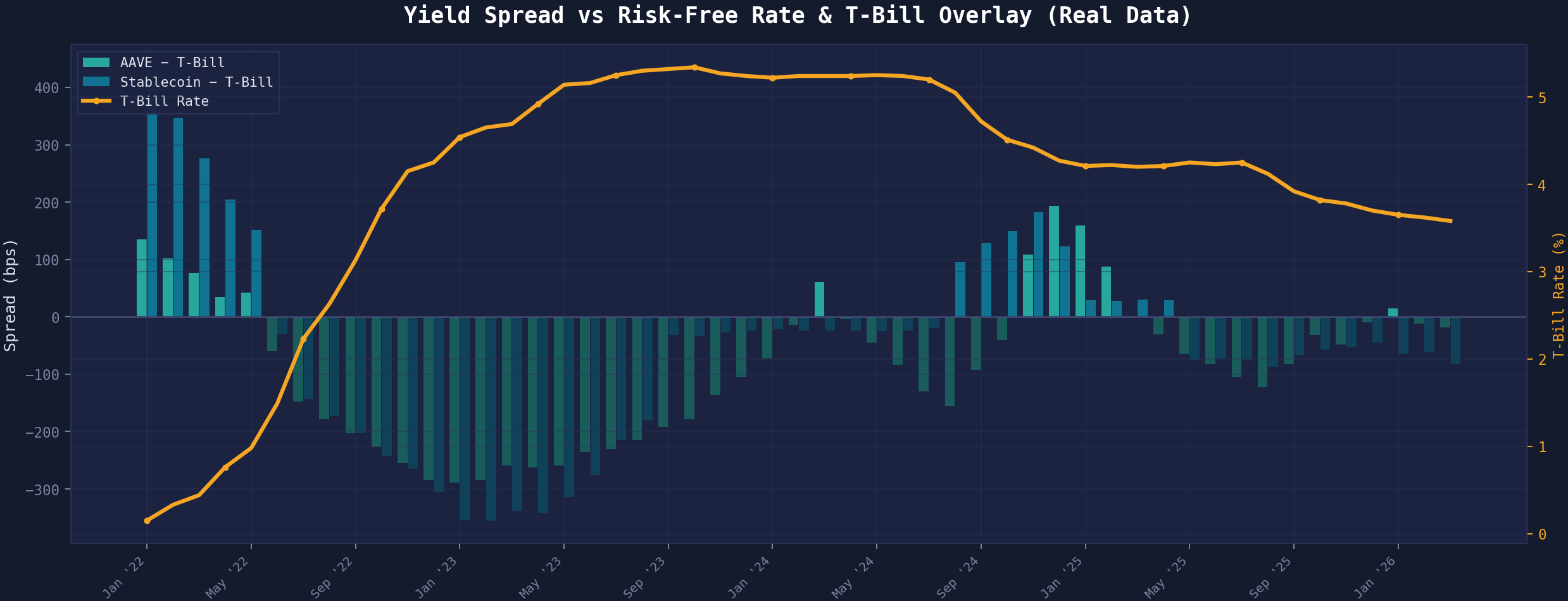

Figure 3: Yield Spread vs Risk-Free-Rate & T-Bill, [Aave-TBill Spread, Stablecoin-TBill Spread, 3-mo T-Bill Yield]

The figure above clearly highlights the structural regime shift in yields. From large spreads in Aave and T-Bill rates in early 2022, to the T-Bill surge, leaving stablecoin yield lacking in late 2020. We observe the 2024 convergence with Aave yields holding within a 50bps spread, while regulatory development keeps stablecoin yield suppressed. The blockchain treasury yield is now treated as a substitute for the T-Bill, priced with a minor on-chain premium.

The Landscape of the Tokenized Asset Class

In theory tokenized assets will enable fractional ownership of assets ranging from stocks to real estate, offer 24/7 market liquidity and allow near-instant settlement. However the current market microstructures reveal that secondary turnover is limited and liquidity is fragmented across asset classes.

The takeaway is simple, not all tokenized assets are created equal. With a market capitalization of approximately $26B, most of the value remains in assets that are not actively traded. Even if an asset can be tokenized, it does not guarantee liquidity.

Tokenized Treasuries and Gold

The most active tokenized asset segments are treasury products and gold, anchored by BUIDL, BENJI and Tether and Paxos's XAUT & PAXG.

BUIDL and BENJI, together represent over $3B in on-chain value with their products evolving past mere yield generation. These products are actively deposited as collateral in lending protocols to borrow stablecoins, which can then be redeployed. This creates capital efficiency loop which directly connects traditional treasury products to on-chain finance.

The Gold market is active primarily through Tether’s XAUT and Paxos’s PAXG. The segment has crossed $6B in total market capitalization with daily trading volumes reaching upwards of $1B during volatile (risk-off) periods. From a trading perspective, this is the most active, high-velocity RWAs market, and is already deeply integrated in DeFi primitives. Tokenized Gold is currently at limited by structural concentration risk. The two main players control upwards of 90% of the market capitalization that increases the risk of an operational failure causing a cascading liquidation event.

Private Credit and Real Estate

Recently, Private Credit has rapidly grown into one of the largest RWA sectors with ~$9B of active on-chain loans and structured debt. However, in trading volumes, it remains one of the least active sectors. Capital here is typically deployed at origination and held until maturity, meaning there is no significant secondary market. When transfers occur, they typically do so via bespoke OTC deals requiring complex legal intervention through multi-sig wallets, KYC and AML verifications. This process can be very timely, a stark contrast of atomic settlement tokenization is known for.

The Real Estate market sees ~370M in tokenized property across more than 10,000 holders, but only ~400 monthly trading wallets. The asset remains highly illiquid, reflecting its real world equivalent. While transfer of ownership is more traceable, tokenizing an illiquid asset is not the cure for liquidity.

Understanding the On-Chain Premium

On-chain representations of products are typically priced higher than their real life counterparts (lesser yields), but why?

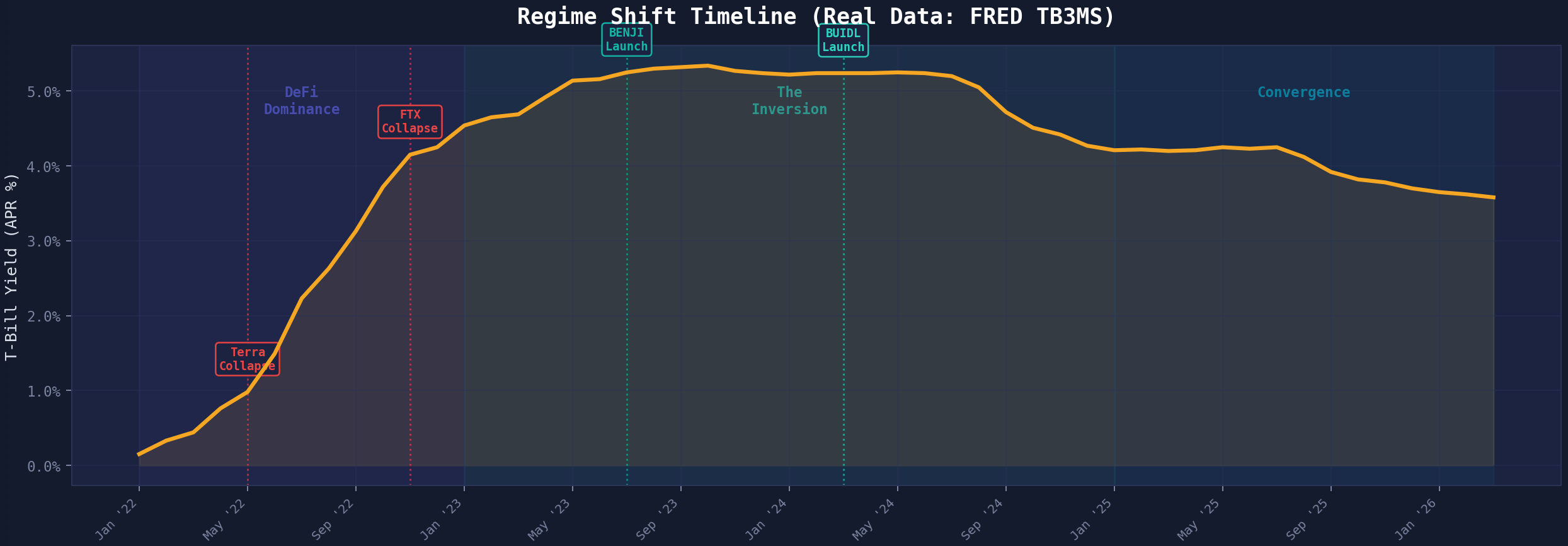

We see in the figure below how RWAs have taken the place of uncollateralized yield-bearing instruments in the current market structure. 3mo T-Bill yields are plotted across four structural phases of the market from the DeFi dominant era of the 2022s to the current state of convergances. When Terra collapsed in 2022 and FTX later the same year, algorithmic yield models suffered. The market responded by moving to asset backed products, the same products we now know as tokenized treasury products. In 2023 when BENJI launched T-Bill rates exceeded the DeFi yields for the first time in our timeseries, marking a decisive regime shift. We now observe T-Bills easing to a 3-4% yield with tokenized products closely tracking, indicating we have entered a mature market, constrained by arbitrage.

Figure 4: The Regime Shift Timeline

Pricing these RWAs requires a nuanced approach. Purchasing a tokenized asset is not simply purchasing the underlying asset at market price, but paying a small premium that reflects the cost of additional layers required to bring the asset on-chain. The asset price remains anchored to its real world equivalent, Tokenized Treasuries track the T-Bill, XAUT tracks Gold spot. The price traded on-chain includes the "on-chain premium", a spread reflecting the fund's management fee, the cost of redemption to the underlying and any time and legal enforceability of your claim. Typically this premium is small, ~10-20bps for liquid products, but can rise to 1-5% for illiquid assets such as Real Estate which are valued upon appraisal rather than live market prices.

Looking to the Future

Tokenized RWAs offer opportunities for investors of any scale. An investor in Amsterdam can now easily trade tokenized treasuries earning the same yield that was previously restricted to brokerage accounts and money market funds. An investor in Asia can now hold a fractional tokenized equity position without a traditional intermediary. RWAs are lowering the barrier to entry that have traditionally outcast smaller investors, geographic restrictions and trading hours.

The first wave of RWA has been defined by Gold and Treasury products. Tokenized equity will define what comes next. On March 9, 2026, Kraken and Nasdaq announced a partnership to distribute 1:1 tokenized stocks to investors internationally. Token holders, under this agreement will keep the shareholder rights of traditional equities including voting rights and dividends. This announcement builds upon the 2025 acquisition of the company behind xStocks, a product allowing investors to trade 1:1 in backed tokenized equities 24/7.

The Intercontinental Exchange (ICE) has recently invested into OKX at a $25B valuation with plans to offer tokenized stocks and crypto futures products.

The crypto industry is continuously evolving and maturing. With the growth of RWAs we now have a stable yield bearing asset not driven by speculation. TradFi and DeFi are converging in real time, rewriting market microstructure and broadening the investment opportunities of every investor.

THE CONTENT ON THIS WEBSITE IS NOT FINANCIAL ADVICE

The information provided on this website is for information purposes only and does not constitute investment advice with respect to any assets, including but not being limited to, commodities and digital assets. This website and its contents are not directed to, or intended, in any way, for distribution to or use by, any person or entity resident in any country or jurisdiction where such distribution, publication, availability or use would be contrary to local laws or regulations. Certain legal restrictions or considerations may apply to you, and you are advised to consult with your legal, tax and other professional advisors prior to contracting with us.